Legal documents

Comun Account Terms & Conditions

(the “Agreement”)

Effective as of November 21st, 2025.

IMPORTANT – Please read carefully and retain this Agreement for your records.

Your Comun Account, and its respective debit card (each an “Account” and a “Card,” as further defined below) is offered by Community Federal Savings Bank (“CFSB” or “Issuing Bank Partner” or “Sponsor Bank” or “Bank”), an FDIC insured depository institution, and is distributed and serviced by Comun, Inc. (“Comun”) on behalf of the Bank. “We,” “us,” and “our” means Bank and its successors and assigns.

If you have any questions about this notice, please contact ayuda@comun.app.

Terms and Conditions

This Agreement contains the rules that govern your Account(s) and Card(s) where appropriate.The funds in your Comun Account(s) are held at CFSB, member FDIC. Your Card is issued by CFSB, pursuant to a license by Visa U.S.A. Inc. This Agreement is subject to applicable federal laws and the laws of the State of New York.

Definitions

- An Account (also referred to as a Deposit Account) refers to an arrangement by which the Bank accepts Your deposits and holds them on Your behalf at their discretion.

- A Card refers to the Comun Visa debit card, which is issued by CFSB in the name of the Cardholder for carrying out all Card Transactions from an Account, as provided for in this Agreement.

- A Cardholder is the person in whose name an Account has been opened and in whose name a Card is issued.

- Card Transactions are any payment made for goods or services, cash withdrawals from a bank or financial institution (including ATM withdrawals) or transfer of funds made through the use of the Card or the Card number.

- A Disclosure is a document provided by Comun that outlines all pertinent information about a product or service. A Disclosure is typically provided at Account opening or when a change in the terms of the account occurs.

- Financial Services refer to a Deposit Account, Bill Payment service, Funds Transfer service, or any other financial product or service available through Comun.

- A Mobile Deposit is the ability for an Owner to deposit a check via Comun’s App by snapping a picture of the front and back of a physical check using their smartphone. In traditional banking, these digital transactions are known as remote check deposits.

- Non-Personal Accounts (which must be distinguished from their counterpart, Personal Accounts) are Accounts in the name of corporations, partnerships, trusts, and other entities.

- An Owner is one who has the power to manage or control an Account in their own name.

- Personal Accounts are Accounts in the names of natural persons (individuals).

- You (or Your) refers to each Account Owner and anyone else with authority to deposit, withdraw, or exercise control over an Account. If there is more than one owner, then these words mean each Account Owner separately and all Account Owners jointly.

Consent to Terms and Conditions and Modifications

By enrolling in services or applying for an Account through Comun’s platform, you agree to be bound by these Terms and Conditions of the Account and any fees that may be imposed. The Terms and Conditions of your Account include this Agreement, any disclosures we give you when you open your Account, subsequent disclosures we provide when using additional products and services, periodic statements, user guides, our Privacy Policy, which can be found at https://www.cfsb.com/privacy and is part of this and any other disclosure or terms we provide to you. Continued use of your Account means you agree to these terms, you agree to pay the fees listed, and you give us the right to collect the fees, as earned, directly from your Account balance or any linked external Accounts.

Modifications

We may amend or change any terms of this Agreement or any Account disclosures and documents provided to you. Notice of the amendment or change will be provided to you as required under applicable law.If at any time the terms, conditions or fees associated with your Account are not acceptable to you, you may terminate this Agreement by closing your Account after paying any fees or charges owed to us. We may cancel or suspend your Account, Card, or other Account services, or this Agreement at any time.

Business Days

For purposes of these disclosures, business days are Monday through Friday, unless stated otherwise. Federal holidays are not included.

Identification Notice (USA PATRIOT ACT)

To help the government fight the funding of terrorism and money laundering, Federal law requires all financial institutions to obtain, verify, and record information that identifies each person who opens an Account.This means that when you open an Account or use our services, we may ask for your name, physical address, date of birth, and other information that will allow us to identify you. We may also ask to see other identifying documents such as driver’s license or other documents that validate your identity.Even if you have been an existing customer of ours, we may ask you to provide this kind of information and documentation because we may not have collected it from you in the past or we may need to update our records.If, for any reason, any Owner is unable to provide the information necessary to verify their identity, their Account(s) may be blocked or closed, which may result in additional fees assessed to the Account(s).You are responsible for the accuracy and completeness of all information supplied to Comun or the Bank in connection with your Account and/or Account services and for keeping your personal data with us updated if you move or otherwise make changes to your personal data.

General Terms and Conditions

Who Can Use the Service

Only individuals 18 years of age or older who can form a legally binding contract and have a valid residential address in the United States can use our Services. We may impose other restrictions as well.

Personal Accounts

An Account opened for personal use cannot be used for business purposes. If your personal Account is identified as being used as a business Account, business-related transactions will be reversed, your Account privileges will be suspended, and your Account may be closed if business related activities continue.

Community Federal Savings Bank

Comun is a fintech company and not a bank. Comun has partnered with CFSB, an FDIC insured financial institution, to offer you certain banking services through Comun’s platform. When you sign up for an Account, you will be prompted to agree to CFSB’s Privacy Notice. You authorize us to share any of your information with Comun for the purposes of establishing and administering your Account. It is your responsibility to make sure the data you provide to us is accurate and complete. Before opening your Account, You must accept CFSB’s Privacy Policy, which can be found at https://www.cfsb.com/privacy and is part of this Agreement.Your funds are eligible for FDIC deposit insurance up to the applicable limits provided by law (the current FDIC deposit insurance limit is $250,000 for each account ownership category).In the event of Bank’s failure, your funds, aggregated with any other funds you have on deposit at the Bank, would be eligible to be insured by the FDIC up to $250,000 for each account ownership category. You are responsible for monitoring the total amount of deposits (including non-Comun accounts) held by you at the Bank for purposes of determining the amount of your deposits that may be eligible for FDIC deposit insurance.Any amount of your deposits at the Bank that exceeds the $250,000 insurance limit may be uninsured.Comun will provide you with any and all notifications as well as all customer support related to your Account.If you have any questions, please contact us at ayuda@comun.app.

Connected Accounts

To ensure a more valuable experience with us, Comun uses Plaid Technologies, Inc. (“Plaid”) to gather your data from external financial institutions you connect via the Comun App. By using your Account, you grant Comun and Plaid the right, power, and authority to act on your behalf to access and transmit your personal and financial information from the relevant financial institution(s). You agree to your personal and financial information being transferred, stored, and processed by Plaid in accordance with the Plaid Privacy Policy at plaid.com/legal. Comun’s use of Plaid is unrelated to the Bank.

Account Balances

You agree to maintain a positive balance and will not incur overdrafts. If you manage your Account in such a way that it results in a negative balance or your account becomes overdrawn, you agree to rectify the matter by transferring sufficient funds to your account to pay the overdrawn balance. Your failure to bring your Account to a positive balance could result in the temporary or permanent suspension of your Account and services. Further consequences may be enacted if you do not remedy the situation in a timely manner and may include (1) freezing your Account until the negative balance is rectified, (2) the reporting of your negative balance to a reporting agency, and/or (3) legal action.

Confidentiality

We will disclose information about your Account or the transactions you make to third parties:

- When it is necessary to complete transactions;

- To verify the existence and standing of your Account with us upon the request of a third party, such as a credit bureau or merchant;

- In accordance with your written permission;

- In order to comply with court, governmental, or administrative agency summonses, subpoenas, or orders;

- On receipt of certification from a federal agency or department that a request for information is in compliance with the Right to Financial Privacy Act of 1978.

Account Closing

If you wish to close your Account with us, you agree to withdraw all of the funds from your Account. We may require you to notify us of this intention in writing by sending an email to ayuda@comun.app. After an Account is closed, we have no obligation to accept deposits or pay outstanding items. However, we may do so at our discretion. You agree to hold us harmless for refusing to honor any item on a closed Account. If funds remain in the Account after you have notified us of your intent to close your Account, we will require you to submit your request to us in writing by sending an email to ayuda@comun.app, and we will then return any remaining funds to your linked external Account. All related closing fees will be deducted from the final balance.

Inactive and Dormant Accounts

We may consider a Deposit Account to be inactive after a period of no owner-initiated activity of 120 days. After the Account has been deemed inactive, we may consider a Deposit Account to be dormant, at which time it will be closed. However, if we close your Account for inactivity, state escheat laws may, depending on the length of the inactivity, require us to transfer your balance to a state agency. If this occurs, you may be able to file a claim with that agency to recover the funds.If the Account becomes inactive or dormant, the Account will continue to be subject to any service charges in accordance with our Schedule of Fees and Charges. If an Account becomes inactive, we will notify you with specific instructions on how to restore the Account to an active status without the need to make any transactions.

Death or Incompetence

You or your appointed party, designee, or appointed individual agree to notify us promptly if any person with signatory rights on your Account dies, becomes legally incompetent, or incapacitated. We may continue to honor any items submitted until (i) we know of the fact of death or of a legal determination of incompetence or incapacitation and (ii) we have had a reasonable opportunity to act on that knowledge. You agree that, even if we have knowledge of the death of a person with signatory rights, we may pay on items drawn on or before the date of death for up to ten (10) days after that date, unless ordered to stop payment by someone claiming an interest in the Account. We may require additional documentation to confirm any claims made on the Account.

Levies, Garnishments, and Other Legal Processes

If your Account becomes subject to legal action, such as a tax levy or third-party garnishment, we reserve the right to refuse to pay any money from your Account, including checks or other items presented for payment, until the action is resolved. If we are required to pay an attachment, garnishment, or tax levy, we are not liable to you. Payment is made after satisfying any fees, charges, or other debts owed to us. You agree that you are responsible for any expenses, including legal expenses and fees we incur due to a garnishment, levy or attachment on your Account. We may charge these expenses to your Account. Until we receive the appropriate court documents, we may continue to process transactions against your Account, even if we have received an unofficial notification of an adverse claim. You will indemnify us for any losses if we do this.

Withdrawals from Accounts

Unless otherwise indicated by us, anyone who is listed as an Account Owner, may withdraw or transfer all or any part of the Account balance at any time on forms approved by us or with your debit card, through Bill Pay, or other available services.You may use the Card to purchase goods or services everywhere Visa debit or Maestro cards are accepted. With the PIN, you may use your Card to withdraw cash from your Account at any ATM or Point-of-Sale device (if cash-back functionality is made available by the merchant) that bears the Visa or Maestro acceptance marks. All ATM transactions are treated as cash withdrawal transactions.We reserve the right to refuse any withdrawal or transfer request that is attempted by any method not specifically permitted, that exceeds any frequency or monetary limitations, or where we suspect fraudulent or unlawful activity. Even if we honor a nonconforming request or allow a transaction or transaction(s) to overdraw your Account, repeated abuse of the stated limitations, or regularly overdrawing your Account, may force us to close the Account. We will use the date a transaction is completed by us (as opposed to the day you initiated it) to apply the frequency limitations.

Deposits to Accounts

All items deposited will be handled by us as an agent for you. We accept check deposits select eligible Accounts in accordance with applicable terms and conditions. We accept cash deposits through Allpoint. We do not accept third-party checks (checks not made payable to you). We do not accept deposits in foreign funds or checks drawn on banks outside the United States. We reserve the right to reject a deposit if it is made payable to CFSB or Comun and contains no other information that might assist us in identifying the Account to which it should be deposited. We reserve the right to refuse any other type of deposit if we believe it is fraudulent, will not be paid, it is not made payable to you only, or is otherwise suspicious in nature. We will not be held liable if such action causes outstanding items to be dishonored and returned or payment orders to be rejected. Refused deposits will be returned to you.

Automated Clearing House Deposit

In order to transfer funds from an account that you own or have control of at another financial institution to your Account at the CFSB using the Automated Clearing House (ACH) Funds Transfer service, Plaid will be used to gather your data from the external financial institution(s) you connect via the Comun App. By using our service, you grant Comun and Plaid the right, power, and authority to act on your behalf to access and transmit your personal and financial information from the relevant financial institution(s). You agree to your personal and financial information being transferred, stored, and processed by Plaid in accordance with the Plaid Privacy Policy at plaid.com/legal. ACH transactions will not be processed and accessible until the service is activated by us. Funds from these types of deposits will not be available until after the funds have settled.

Cash Deposits

We accept cash deposits to your Comun account in conjunction with designated merchants through Incomm Vanilla Reload. Your Cash Load limit is a total of $1,000 per day and a total of $10,000 per monthly statement period. Please do not send cash deposits through the mail. In the event that a cash deposit is received for your Account, you agree that Comun’s determination of the amount of the deposit will be final. We are not liable for any deposits, including cash, lost in the mail, lost in transit, or not received by us.

Direct Deposits

You may initiate direct deposits by providing your employer or government benefits administration with our Routing Number and your Account number, which can be found by logging in to the Comun App. If we deposit any amount into your Account which should have been returned to the Federal Government for any reason, you authorize us to deduct the amount of our liability to the Federal Government from your Account or from any other Account(s) you have with us, without prior notice and at any time, except as prohibited by law. We may also use any other legal remedy to recover the amount of our liability.If a direct deposit posts to your Account and is later found to be made payable to someone other than yourself or another Account Owner listed in our records, the amount of the deposit will be deducted from your Account and returned to the originator without prior notice to you.

Foreign Transactions

If you make a purchase using your Card or Account in a currency other than in U.S. dollars, the amount deducted from the available funds in your Account will be converted by Visa into U.S. dollars. The applicable exchange rate will be selected by Visa from the range of rates available in wholesale currency markets for the applicable central processing date, which may vary from the rate Visa itself receives or the government-mandated rate. The exchange rate used on the central processing date may be different from the rate that was in effect on the date you performed the transaction.

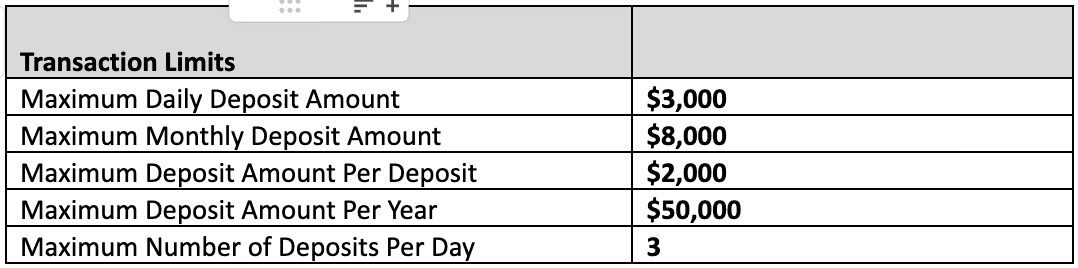

Transaction Limits

The following transaction limits apply to your Comun Account:

* The recipient’s name on any direct deposit or ACH transfer must match the name on the Account or the deposit may be returned to the originator or rejected.

** You may transfer funds between your Account and another external bank account. The connected bank account must be located in the United States

*** We may adjust these limits in our sole discretion at any time and for any reason. We will notify you of any changes, as required by law.

Mobile Wallet

When you or a Cardholder adds a Card to a mobile wallet, you agree to the following terms:

- A Card can be added to a mobile wallet by following the instructions of the mobile wallet provider (ApplePay, GooglePay, SamsungPay, etc.). A Card can be added to multiple mobile wallets and on multiple devices as long as it is eligible to do so. This Agreement, and the terms of the mobile wallet provider and any service providers (e.g., third-party wireless companies) apply to a Card in a mobile wallet regardless of which mobile wallet it is added to. No Card can be used in a mobile wallet if the Card has been canceled.

- The terms and conditions of this Agreement do not change when a Card is added to a mobile wallet. In addition, any applicable fees that apply to your Account apply to activity done through a mobile wallet as well.

- When a Card is added to a mobile wallet, it can be used to make purchases wherever mobile wallets are accepted. Mobile wallets may not be accepted everywhere that a Card is accepted.

- If any Cardholder uses a mobile wallet, you agree to protect and keep confidential your User ID, passwords and all other authentication information required for use of the Card in a mobile wallet.

- All questions or complaints about mobile wallet-specific functions or security should be directed to the mobile wallet provider. All transaction-related questions should continue to be directed to Comun.

Deposited Items Returned

If final payment is not received on any item you deposited to your Account, or if any direct deposit, ACH deposit, or Electronic Fund Transfer to your Account is returned to us for any reason, you agree to pay us the amount of the return.We may charge any Account of which you are an owner or re-present any item you deposit with us that is returned to us unpaid without prior notice to you. We may charge a fee for returned deposited items in accordance with our Schedule of Fees.You authorize us to attempt a collection of previously returned items that you deposited. In our attempts to collect these items, you agree that we may allow the payor bank (the bank on which the item is drawn) to hold the item beyond its midnight deadline. If an item you deposit is returned unpaid, you waive the requirement for notice of this return.If a claim is made on any item subsequent to final payment on the grounds that the item was altered, bears a forged or unauthorized endorsement, or was not otherwise properly payable, we may withhold credit for the item from your Account until final determination of the claim. In addition, we will not be liable for a check, draft, or other item that you deposit that has been forged or altered in such a way that a reasonable person could not discover the forgery.

Funds Availability Policy

Information contained in this section is to assist you in understanding our Funds Availability Policy. Comun does not accept in-person or mailed deposits.It is our policy to review each deposit and determine how the funds are being deposited. We make the funds available to you according to the deposit type and when the funds are applied to your Account. Some deposit types may not be available for immediate use. When we delay the availability of funds or place a hold on a deposit made to your Account, you may not withdraw those funds, and we will not use them to pay bills or other debits, such as ACH withdrawals during the hold period.We reserve the right to refuse any deposit. If final payment is not received on any item you deposited to your Account, or if any direct deposit, ACH deposit or Electronic Fund Transfer to your Account is returned to us for any reason, you agree to pay us the amount of the return, plus any fee in accordance with our Schedule of Fees and Charges.

Availability

The length of delay in the availability of funds varies depending on the type of deposit. Special rules may apply to new Accounts.

Business Days

The length of delay in the availability of funds is counted in business days from the day your deposit is applied to your Account. Deposits received after 5:00 PM (CST) will be considered to be received on the next business day.

Same-Day Availability

Funds from wire transfers, transfers between Comun Accounts, preauthorized electronic payments such as payroll direct deposits, or other preauthorized electronic payments will be available on the day the deposit is applied to your Account.Funds from ACH credits received from an external bank account or transfers initiated by the customer will be applied to the Account when we have verified the external Account and received payment on collected funds. Once the funds are applied to your Account, they will have same-day availability.

Longer Availability

Electronic transfers depositing into your Account initiated through the Mobile App may take up to five (5) business days from the date of the initial request but will post on the payment date of the deposit once the money has reached the Bank.

Card Activation

You must activate your Card in accordance with the instructions provided with your Card before it can be used. You will need to activate your card via Comun’s mobile app or reach out to our customer support team.

ATM and Debit Card Transactions

Consistent with applicable law, you may use your Card with your signature or PIN to perform most routine transactions on the Accounts that are accessible by your Card, such as to:

- Make cash withdrawals;

- Obtain your most recently available Account balance;

- Pay for purchases at places that have agreed to accept the card.Some of the above services may not be available at all ATMs or locations.

Authorized Card Users

You are responsible for all authorized transactions initiated and fees incurred by use of your Card. If you permit another person to have access to your Card or card number, we will treat this as if you have authorized such use and you will be liable for all transactions and fees incurred by those persons. You are wholly responsible for the use of each Card.

International ATM Transactions

International transactions made using your Card will be converted to U.S. currency according to the rules and regulations of the card network. The conversion of the currency to U.S. currency may occur on a date other than your original transaction date and fees may be assessed by these networks. You are responsible for the U.S. currency amount plus any fees assessed for the currency conversion. Some services may not be available at international ATM terminals. International ATM transactions may be subject to a fee in accordance with our Schedule of Fees and Charges.

ATM Deposits

We accept cash deposits to your Account in conjunction with designated merchants through Allpoint networks. Your Cash Load limit is set forth in the Transactions Limit table above. Please do not send cash deposits through the mail. In the event that a cash deposit is received for your Account, you agree that Comun’s determination of the amount of the deposit will be final. We are not liable for any deposits, including cash, lost in the mail, lost in transit, or not received by us.

Debit Card Point-of-Sale Transactions

You may use your Card to purchase goods and services and/or obtain cash (where permitted) from any merchant who accepts Visa®. The merchant may require your signature instead of your PIN to authorize the purchase request. You may also use your Card with your PIN at any merchant location where ATM cards are accepted to purchase goods, services, and/or obtain cash. The amount of all purchases, including any cash obtained, will be deducted from your Account. When you make a purchase through the card network, we may place a hold on the funds in your Account in the amount that may be necessary to cover the amount of the transaction. (Please see Preauthorization Holds for additional information.)

Split Transactions

If you do not have sufficient funds in your Account, you can instruct the merchant to charge a part of the purchase to the Card and pay the remaining amount with cash or another card; these are called split transactions. Some merchants do not allow cardholders to conduct split transactions. Some merchants will only allow you to do a split transaction if you pay the remaining amount in cash. If you fail to inform the merchant that you would like to complete a split transaction prior to swiping your Card, the card transaction is likely to be declined.

Transactions Using Your Card Number

If you initiate a transaction without presenting your Card (such as for mail order, internet purchases, telephone purchases, a Prefunded Check purchase, or an ACH debit purchase), the legal effect will be the same as if you used the Card itself.

Limitations on Frequency of Debit Card Transactions and Cash Withdrawal Limits

Frequency-of-use limitations are imposed on card transactions for security reasons and for the protection of your Account. They are not disclosed for this reason and may be changed at any time. You will be denied the use of your Card if:

- You exceed the daily ATM withdrawal or purchase limit;

- You do not have sufficient available funds in your Account;

- You do not enter your correct PIN;

- You exceed the Card purchase limit on your Card each day.The receipt provided by the ATM or merchant terminal will notify you of a denial. There is a limit on the number of denials permitted. Exceeding that limit may cause the ATM to retain your Card. The number of attempts that will cause the retention of your card is also not disclosed for security reasons.

Preauthorization Holds

When your debit card or other network enhancement feature related to the Card is used at a point-of-sale location to obtain goods and services or obtain cash, the merchant may attempt to obtain preauthorization from us for the transaction. We may place a temporary hold on your Account for the amount of the preauthorization request based on the vendor type. This hold can range from two (2) to thirty (30) days (depending on the merchant’s request) and may vary from the amount of the actual purchase in some instances. If the preauthorization request varies from the amount of the actual transaction, payment of the transaction may not remove the hold, which will remain on the Account until the end of the hold period. This hold may affect the availability of funds from your Account to pay checks or for other EFTs. We will not be responsible for damages for wrongful dishonor of any items that are not paid because of the hold.

Electronic Funds Transfer Disclosures

We offer Account services that may be considered Electronic Funds Transfers (“EFTs”), which include, but are not limited to the following:

- ATM Transactions;

- ACH Transactions;

- Card transactions;

- Transfers initiated through the Comun app.This EFT disclosure, as required by Federal Regulation E - Electronic Fund Transfer Act and provides information that describes your rights and responsibilities regarding these services. Electronic Funds Transfers are services that we can provide, assuming that you specifically request and arrange them and qualify for the service.

Preauthorized Electronic Funds Transfers

You may arrange to have certain recurring payments automatically deposited (credited) to your Account. Examples of this service include, but are not limited to the direct deposit of Social Security and other government payments or the direct deposit of your payroll. If you have arranged to have direct deposits made to your Account at least once every sixty (60) days from the same person or company, you can verify the availability of your deposit by viewing the transaction details on your Comun mobile app or contacting us.You may arrange to have certain recurring withdrawals automatically paid (debited) from your Account. For example, you may arrange to have insurance premiums paid automatically.These preauthorized transfers are governed by federal regulations pertaining to EFT services that entitle you to certain protections. Requests for these services must be authorized by you, in writing, to the Originator of the transaction prior to becoming effective.

Right to Stop Payment of Preauthorized Electronic Funds Transfers

If you want to permanently revoke an EFT (either debit or credit) you authorized from a third party, you will need to first send written instructions to the originating third party to cancel your ACH transfer.If you have authorized regular payments out of your Account, you can stop any of these payments by notifying Customer Service by telephone or email. If you notify us by telephone, you may be required to confirm the information provided by writing to us at ayuda@comun.app.Your request must include your Account number, the name of the payee, the amount of the item to be stopped, and the date payment was scheduled to be made. This request needs to be received by us three (3) or more business days before the payment is scheduled to be made. If your request is by telephone or email, we may also require you to put your request in writing and ensure that it is received by us within fourteen (14) days after your call or email.You are subject to the general rules of Stop Payments in this Agreement.

Stop Payments

If you request that we stop payment on any preauthorized transfer according to the requirements above and we fail to do so, we will be liable for your proven loss or damages, unless:

- You failed to give us enough information, proper instructions, or sufficient time to act on the stop payment or

- We do not receive written confirmation of your telephone or email request to stop payment within fourteen (14) calendar days, and the preauthorized transfer occurs after the fourteen (14) calendar days.In any case, we will only be liable for actual proven damages if the failure to stop payment on your transaction resulted from an error on our part, despite our procedures to avoid such errors. If we pay a preauthorized transfer despite your valid and timely stop order request, we may recredit your Account. If we do this, you will sign a statement describing the dispute with the payee. You agree to transfer to us all of your rights against the payee. In addition, you will assist us in any legal action taken against the payee.Additionally, if you want to permanently revoke a recurring preauthorized EFT, you will need to first send written instructions to the originating third party to cancel your preauthorized transfer. We may ask you to provide us with a copy of your letter to the originating third party and sign an Affidavit revoking authorization.

Our Liability for Failure to Complete an Electronic Fund Transfer

If we fail to complete an EFT transaction on time or in the correct amount when properly instructed by you, we will be liable for damages caused by our failure unless:

- There aren’t sufficient funds in your Account to complete the transaction through no fault of ours;

- The funds in your Account aren’t available at the time the EFT posts to your Account.

- The funds in your Account are subject to legal process;

- The ATM system has insufficient cash to complete the transaction;

- Your Card has been reported lost or stolen and you are using the reported Card;

- We have a reason to believe that the transaction requested is unauthorized;

- The failure is due to an equipment breakdown that you knew about when you started the transaction at an ATM or merchant terminal;

- You attempt to complete a transaction at an ATM or merchant terminal that is not a permissible transaction listed above;

- The transaction would exceed security limitations on the use of your Card.In any case, we will only be liable for actual proven damages if the failure to make the transaction resulted from an honest error despite our procedures to avoid such errors.

Unauthorized Transfers

Tell us immediately if you believe your Card and/or PIN has been lost or stolen or if you believe that an EFT has been made without your permission. Contacting us by phone or email is the best way to keep your potential losses down.If you tell us within two (2) business days after you learn of the loss or theft of your Card and/or PIN, you can lose no more than $50 if someone used your Card and/or PIN without your permission.If you do NOT tell us within two (2) business days after you learn of the loss or theft of your Card and/or PIN, and we can prove we could have stopped someone from using your Card and/or PIN without your permission if you had told us, you could lose as much as $500.Also, if your statement shows transfers that you did not make, including those made by card, code or other means, tell us at once. If you do not tell us within sixty (60) days after your Account statement is made available to you, you may not get back any money you lost after the sixty (60) days, if we can prove that we could have stopped someone from taking the money if you had told us in time. If extenuating circumstances kept you from telling us, we may extend the time periods at our sole discretion.You may be required to confirm the information provided over phone or email in writing. In these cases, we will advise you accordingly, provide you the necessary forms for confirming your dispute in writing, and give you instructions for sending us the signed form.

Errors or Questions and How to Contact Us

In case of errors or questions about your Electronic Fund Transfers, you agree to promptly contact Customer Service by telephone (646) 600-5660 or by email at ayuda@comun.app. You may be required to confirm the information in writing within ten (10) business days. In these cases, we will advise you accordingly, provide you the necessary forms for confirming your dispute in writing, and give you instructions for sending us the signed form.If you believe an EFT transaction was processed in error or was unauthorized or if you need more information about a transfer listed on your statement or receipt, you must contact Comun no later than sixty (60) days after the problem or error first appeared on your statement.In your communication, please provide the following information:

- The Account name, Account number, and last four digits of the Card number, if applicable;

- A description of the suspected error or the transfer about which you are unsure, why you believe there is an error, or why you need more information;

- The dollar amount of the suspected error;

- The date of the suspected error.When we receive your dispute notification, we will advise you of the status of our investigation within ten (10) business days. In all cases, we will correct any error promptly.If we need more time to investigate your question or complaint, we may take up to 45 calendar days for ATM transactions (other than international transactions) and ACH transactions. For errors involving new Accounts (an account that was first funded within 30 days prior to the error), point-of-sale transactions, or foreign initiated transactions, we may take up to 90 calendar days to investigate your complaint or question. If this is necessary, we will provisionally credit your Account for the amount you believe is in error within ten (10) business days of your original complaint or question. If we do not receive written confirmation of your questions or complaint within ten (10) business days, we may decide not to provisionally credit your Account.For errors involving new Accounts, point-of-sale, or foreign initiated transactions, we may take up to 90 calendar days to investigate your complaint or question. For new Accounts, we may take up to 20 business days to credit your Account for the amount you think is in error.We will send you a written explanation within three (3) business days after we finish our investigation. You may ask for copies of the documents we used in our investigation. If provisional credit was given, and it is determined that there was no error, you must repay to us the amount of the provisional credit for the disputed item(s). You will have access to those funds for five (5) business days, and then we may deduct those amounts from your Account without further notice.

Card Revocation

You agree that your Card remains the property of CFSB and shall be surrendered upon demand. The Card is non-transferable, and it may be canceled, repossessed, or revoked at any time without prior notice subject to applicable law.If you do not use your Card for 90 days or we believe the Card may be lost, stolen, or used improperly, it may be canceled for security reasons and will be unusable. This may occur without prior notice to you.If your Card is reissued or reactivated, we may charge you a fee for its reissue and/or replacement in accordance with our Schedule of Fees and Charges.

Fees and Charges

You will pay any applicable fees and charges we assess for your Card services and/or other electronic services that you select. Applicable fees will be deducted from your Account and listed on your Account statement. These charges and fees are assessed in accordance with our Schedule of Fees and Charges.You may be charged a foreign transaction fee for point-of-sale purchases made internationally. For ATM transactions, domestic and international, the terminal owner of the ATM may also charge you a fee for use of their ATM. You may, however, be assessed a fee by the card association (for example, Visa) for using your Card at an ATM or making a point-of-sale purchase.

PIN, Passwords, and Passcodes

Card PINYou will be prompted to assign a four (4)-digit card PIN for your Card during Card activation. You may change the PIN at any time by accessing the Card PIN change process through the Comun mobile app.

Password and PasscodeYou will be prompted to establish a password, otherwise known as login credentials, during your Comun platform enrollment. Depending on your mobile application settings, you may be required to enter your full password for subsequent logins to the Comun mobile application to view your Account(s), Card information, and other Comun services. Your Comun password may be changed at any time after you’ve signed into your mobile app session by following the steps for resetting your Password, which are available in Settings. Comun encourages all customers to secure their Comun application using advanced security (e.g. facial recognition).Your login credentials and PIN are identification methods that are both personal and confidential. You are required to use your PIN with your debit card at an ATM or POS merchant terminal. It is a security method by which we help you maintain the security of your Account. Your login credentials are another security method that maintains the security of your Account and the transactions you process through the mobile app.Therefore, you agree to take all reasonable precautions to protect the confidentiality of your login credentials, PIN and/or other access devices. Furthermore, you agree that you will not:

- Reveal your login credentials, PIN, or any other access device information to anyone;

- Write your PIN or login credentials for your card or mobile app down;

- Leave your mobile or other device unattended after you have logged on.

Funds Transfer Service

“Funds Transfer” is an electronic transfer service powered by Plaid that enables you to securely transfer funds from an account at another financial institution to your Account with us, and/or from your Account with us to an account at another financial institution. Prior to use, you are required to register your external bank account for verification and security purposes. Once your Funds Transfer service is active, please refer to the Funds Availability Policy to see when your Funds will be available for your use in your Account. In all cases, funds may be held until we receive verification that the transaction has settled.By using the Funds Transfer Service, you agree that the Bank will transfer funds through ACH services and that the transaction is subject to completion upon our final review and verification. You agree that such requests constitute authorization for such transfers. This authorization is to remain in full force until the Bank has received written notification from you of its termination, you have electronically deleted a registered bank Account or credit card from the Funds Transfer Service, or you have electronically canceled an Account and/or transfers from the Funds Transfer Service in a time and manner that would allow the Issuing Bank Partner and the other financial institution a reasonable opportunity to act on it.This service may be subject to a fee in accordance with our Schedule of Fees and Charges. This service may not be available for all customers and/or Account types.By using the Funds Transfer Service, you are certifying that the registered external accounts that you transfer funds to and from and the debit or credit cards used to transfer from are under the same ownership as the Account with us. If the accounts are not titled the same or ownership among the transferring accounts changes, you will indemnify us for any losses incurred as a result of any transaction you initiate between these accounts that is later returned or is reported unauthorized. If you initiate a transfer that is found to be unverifiable or is unable to be completed for other reasons, you agree to hold us harmless for any loss resulting from the incomplete transfer. If a transfer is made from a third party’s account or registered as an external deposit account before we detect it, we may without notice to you place those funds on hold and debit your Account and return the funds to the third party’s account in the form of a bank check or EFT once we have confirmed the funds cleared the external account.If you use the Funds Transfer Service to transfer funds to or from an Account that has multiple owners, you agree that each owner authorizes the others to (a) register any external bank account, as permitted by the Funds Transfer service, (b) initiate the transfer of funds between your Accounts with us, as permitted by the Funds Transfer service, and (c) initiate the transfer of funds between your Account(s) with us and any registered external bank account. This authority will cease only after we have received and have been given a reasonable amount of time to act on the appropriate documentation needed to change or remove the owner from the Account. Each external bank account owner agrees to be jointly and severally liable to Comun for any losses incurred as a result of the improper use of this service up to and including the transfer amount, any applicable fees, and any legal expenses. Your Funds Transfer request will only be completed if you have sufficient funds in the account from which you wish to transfer funds and the Accounts are linked for transfer capabilities. Funds Transfer transactions are subject to dollar amount limitations, which are determined by us and may be set according to your Account type and/or the type of Funds Transfer Service you are using. These limitations are set for security reasons and are not disclosed for that reason.We reserve the right to limit the number of external accounts that can be linked to your Account for purposes of transferring funds; to limit functionality of the Funds Transfer Service by imposing limits, holds, or other measures; and to close your Account if unlawful activity is found or suspected.

Truth in Savings

The Account is a non-interest bearing account. No interest will be paid.There is no minimum opening deposit requirement to open an Account. You may deposit any amount you wish when opening an Account, however, the Account will remain in a new account status until thirty (30) days after the Account has received a posted deposit.There are no maintenance fees on Accounts. There is no minimum balance required in the Account.

Fees

Fees are charged in accordance with our fees outlined below. If we assess a fee for any other service or make a change to our Schedule of Fees and Charges, we will let you know in advance.To the extent you access our Services through a mobile device, your wireless service carrier’s charges, data rates, and other fees may apply.

*Dollarized Countries are defined as the following: Costa Rica, Ecuador, El Salvador, Nicaragua, Panama, Uruguay.

¹Comun may offer you a lower International Remittance Fee, at our sole discretion. You can review your fee before you confirm your transfer request.

Rights to Setoff

If you owe us (or Comun) any amount, you give us a security interest in your Account. You also give us the right, to the extent not prohibited by law, to set off against your funds to pay the amount owed to us. You agree that the security interest you have given us is consensual and is in addition to our right to setoff. If we exercise our right to set off, we will notify you to the extent required by law.

Taxes

You are responsible for reporting any required Account information to tax authorities and paying any taxes related to your Account.

Severability

If any provision of these Terms is found unenforceable, then that provision will be severed from these Terms and not affect the validity and enforceability of any remaining provisions.

Invalidated Provisions

If an arbitrator or court finds any provision of this Agreement to be invalid, you and the Bank agree that the arbitrator or court should give valid effect to the intention of that provision, and that the remainder of the terms remain in full force and effect.

Dispute Resolution

Governing Law

This Agreement will be governed according to the laws of the State of New York, and all activities performed in connection with our services will be deemed to have been performed in the State of New York. Any controversy, dispute, or claim arising out of or relating to our services or this Agreement will be governed by and construed in accordance with the laws of the State of New York, except the provisions concerning conflicts of law.

Disputes

If a dispute arises between you and the Bank (or Comun), our goal is to learn about and address your concerns, so please send a message to ayuda@comun.app. If we are unable to address your concerns to your satisfaction, we will seek to provide you with a neutral and cost-effective means of resolving the dispute quickly.

Arbitration

THIS AGREEMENT REQUIRES ALL DISPUTES BE RESOLVED BY WAY OF BINDING ARBITRATION.Except for disputes that qualify for small claims court, all disputes arising out of or related to this Agreement or any aspect of the relationship between you and the Bank (or Comun), whether based in contract, tort, statute, fraud, misrepresentation or any other legal theory, will be resolved through final and binding arbitration before a neutral arbitrator instead of in a court by a judge or jury and you agree that the Bank and you are each waiving the right to trial by a jury. You agree that any arbitration under this Agreement will take place on an individual basis; class arbitrations and class actions are not permitted, and you are agreeing to give up the ability to participate in a class action. The arbitration will be administered by the American Arbitration Association ("AAA") under its Consumer Arbitration Rules, as amended by this Agreement.The Consumer Arbitration Rules are available online at: [suspicious link removed].The arbitrator will conduct hearings, if any, by teleconference or videoconference, rather than by personal appearances, unless the arbitrator determines upon request by you or by the Bank that an in-person hearing is appropriate. Any in-person appearances will be held at a location which is reasonably convenient to both parties with due consideration of their ability to travel and other pertinent circumstances. If the parties are unable to agree on a location, such determination should be made by the AAA or by the arbitrator. The arbitrator's decision will follow the terms of this Agreement and will be final and binding. The arbitrator will have authority to award temporary, interim or permanent injunctive relief or relief providing for specific performance of this Agreement, but only to the extent necessary to provide relief warranted by the individual claim before the arbitrator. The award rendered by the arbitrator may be confirmed and enforced in any court having jurisdiction thereof. Notwithstanding any of the foregoing, nothing in this Agreement will preclude you from bringing issues to the attention of federal, state or local agencies and, if the law allows, they can seek relief against the Bank for you.If any portion of this Arbitration Provision is deemed invalid or unenforceable, such a finding shall not invalidate any remaining portion of this Arbitration Provision, this Agreement, or any other agreement entered into by you with us. However, notwithstanding any language in this Arbitration Provision or this Agreement to the contrary, the Class Action Waiver is not severable from the remainder of this Arbitration Provision and, in the event that the Class Action Waiver is held to be invalid and unenforceable, and subject to any right of appeal that may exist with respect to such determination, any class action or representative proceeding shall be determined in a court of law and will not be subject to this Arbitration Provision.IF YOU DO NOT AGREE TO THE TERMS OF THIS ARBITRATION PROVISION, DO NOT USE THE ACCOUNT. CALL (646) 600-5660 TO CLOSE THE ACCOUNT.

Contact Information

We want to hear your comments, concerns, suggestions, or questions. Email us at ayuda@comun.app.

ADDENDUM A: Comun Mobile Deposit Service

IMPORTANT – Please read carefully and retain these terms and conditions for your records.

As a subscriber to the Comun Mobile Deposit Service (the "Service") this Addendum ("Addendum") amends and becomes a part of the Comun Account Terms & Conditions (the "Account Agreement") between you and Community Federal Savings Bank (“CFSB” or “Issuing Bank Partner” or “Sponsor Bank” or “Bank”) an FDIC insured depository institution, serviced by Comun, Inc. (“Comun”) as Program Manager. The terms of the Account Agreement is hereby ratified, affirmed and incorporated herein and shall continue to apply in all respects, as amended hereby. By accepting this Addendum, you agree to this Addendum. In the event of a conflict between this Addendum and the Account Agreement, this Addendum will govern.

General

This Addendum to the Account Agreement between you and the Bank sets forth the terms and conditions of the Service, which allows you to make single item check deposits to an eligible account electronically by using a supported mobile device with a camera to create an image of a paper check and transmitting it and the related deposit data to us using the Comun Mobile Banking app (a "Mobile Deposit").Except as expressly provided in this Addendum, deposits made through the Service are subject to all limitations and terms set forth in the relevant Account Agreement governing your deposit account as it may be modified from time to time, including, but not limited to, those related to deposit acceptance, crediting, collection, endorsement, processing order and errors.

Service Requirements

Use of our Service requires that you have an internet enabled iOS or Android device with a camera and have downloaded our latest version of the Mobile Banking app. In order to enroll in the Service, you must meet the eligibility criteria for the Service as determined by Comun and have an active Account. Eligibility includes, but not limited to, being an existing customer of Comun with an active checking account. A minimum length of such an existing customer relationship with Comun may also apply.

Limitations of Service

When using the Service, you may experience technical or other difficulties. Comun and the Bank cannot assume responsibility for any technical or other difficulties or any resulting damages that you may incur. Comun and Bank reserves the right to change the qualifications of the Service at any time without prior notice. Comun and Bank has the right to reject any check or item transmitted for using the Service without any liability to you. Comun and Bank are not liable for any checks or items it does not receive or for any images that are not readable. Comun and Bank shall have no liability for any alterations to the check or item after they have been transmitted to it by you. Comun and Bank reserves the right to change, suspend or discontinue the Service, in whole or in part, or your use of the Service, in whole or in part, immediately and at any time without prior notice to you.

Eligible Checks

You agree to scan and transmit only "checks" as that term is defined in Federal Reserve Regulation CC ("Reg CC"), with the exception of United States Postal Service money orders; and only those checks that are permissible under this Addendum or such other items as we, in our sole discretion, elect to include under the Service ("Eligible Checks"). You agree that the image of the check transmitted to us shall be deemed an "item" within the meaning of Article 4 of the applicable Uniform Commercial Code.

Image Quality

The image of a check or item transmitted to Comun using the Service must be legible. The image quality of the checks and items must comply with the standards established from time to time by the American National Standards Institute, or any higher standard set by us, and with any requirements set by the Federal Reserve Board, any regulatory agency with jurisdiction over us, or any clearing house the Bank uses or agreement Comun or the Bank has with respect to processing Checks. You agree that Comun and the Bank shall not be liable for any damages resulting from a check or item's poor image quality, including those related to rejection of or the delayed or improper crediting of such a check or item, or from any inaccurate information you supply regarding the check or item.

Deposit Cut off Times

You may access the service anytime 7 days a week. If Comun receives a mobile deposit on or before 7:00 p.m. Eastern Standard Time on a Business Day, Comun will consider that day to be the "Deposit Date". If Comun receives a scanned Item after 7:00 p.m. Eastern Standard Time or on a weekend or a federal holiday, the next Business Day will be the Deposit Date.

Funds Availability

In accordance with Comun's Funds Availability Policy, Mobile Deposit funds will generally be available on the fifth Business Day after the Deposit Date. Longer delays may apply, as specified in the Account Agreement. Mobile Deposit funds may be subject to an uncollected funds hold. If a hold is placed on a Mobile Deposit, you will be notified in accordance with the Account Agreement.

Your Responsibilities, Promises and Warranties to Us

- You will only deposit Eligible Checks through the Service.

- You will submit check images that meet Comun's image quality standards.

- You will not transmit an image or images of the same check to us more than once and will not deposit or negotiate, or seek to deposit or negotiate, such check or item with us or any other party.

- You agree that you will not use the Service to deposit any checks as set forth below:

- Checks payable to any person or entity other than you, or to you and another party

- Checks containing an alteration to any of the fields on the front of the check or item (including the MICR line), or which you know or suspect, or should know or suspect, are fraudulent or otherwise not authorized by the owner of the account on which the check or item is drawn

- Checks previously converted to a substitute check, as defined in Regulation CC as a paper reproduction of an original check that -

- Contains an image of the front and back of the original check;

- Bears a MICR line that, except as provided under ANS X9.100-140 (unless the Board by rule or order determines that a different standard applies), contains all the information appearing on the MICR line of the original check at the time that the original check was issued and any additional information that was encoded on the original check's MICR line before an image of the original check was captured;

- Conforms in paper stock, dimension, and otherwise with ANS X9.100-140 (unless the Board by rule or order determines that a different standard applies); and

- Is suitable for automated processing in the same manner as the original check

- Checks drawn on a financial institution located outside the United States

- Checks not payable in United States currency

- Checks that are remotely created checks, as defined in Regulation CC as a check that is not created by the paying bank and that does not bear a signature applied, or purported to be applied, by the person on whose account the check is drawn

- Checks dated more than 6 months prior to the date of deposit

- Checks on which a stop payment order has been issued or for which there are insufficient funds

- Checks or items drawn or otherwise issued by you or any other person on any of your accounts or any account on which you are an authorized signer or joint account holder (if applicable)

- Checks by the Postal Office otherwise known as a Postal money order

- Cashier’s checks

- Traveler’s checks

- U.S. Savings bonds

- All information you provide to Comun is accurate and true, including that all images transmitted to Comun accurately reflects the front and back of the check or item at the time it was photographed.

- You will comply with this Addendum and all applicable rules, laws and regulations.

- You agree to indemnify and hold harmless Comun and the Bank from any loss for breach of the provisions set forth in the Account Agreement.

- In addition, you agree that if we suffer a loss or expense or otherwise pay out any funds as a result of your breach of any provisions of this Addendum or the Account Agreement, we may debit any account(s) you maintain with the Bank for the amount of such loss or expense or other pay out of funds.

Check Handling Procedures

You agree to follow any and all other procedures and instructions for use of the Service as Comun may establish from time to time:

- Before transmission, you agree to restrictively endorse any check or item transmitted through the Service as "For mobile deposit at CFSB" or as otherwise instructed by Comun or the Bank. After the Item has been scanned and submitted for deposit, you shall not otherwise transfer or negotiate the original Item, substitute check or any other image thereof.

- Comun will acknowledge that it has received an item or check but such acknowledgement does not mean that the check or item contains no errors or has been accepted and that any such check or item will only receive provisional credit. After a check or item has posted to your account, you agree to prominently mark the original check or item as "Deposited" and state the date.

- You agree to destroy or otherwise properly dispose of checks and items that have been accepted for deposit through the Service after 14 days to ensure that such checks and items are not represented for payment and, prior to disposal or destruction, to safeguard such checks and items.

- You agree to promptly supply any information in your possession that Comun requests regarding a check or item deposited or attempted to be deposited through the Service including the original check or item.

Fees

The Service is provided at no charge to you. Comun may, upon at least 30 days prior notice to you, to the extent permitted by applicable law, charge a fee for use of the Service. If you continue to use the Service after the fee becomes effective, you agree to pay the service fee that has been disclosed to you, as may be amended from time to time.

Deposit Limits

Comun reserves the right to impose the following limits on the amount(s) and/or number of Mobile Deposits (over a period of time set by us) that you transmit using the Service and to modify such limits from time to time.

Nothing in this Addendum should be construed as requiring Comun to accept any check or item for deposit, even if Comun has accepted that type of check or item previously. Nor shall Comun be required to identify or reject any Checks that you may submit through the Service that fail to meet the requirements of this Addendum.

Changes to the Service

Comun and Bank reserves the right to terminate, modify, add and remove features from the Service at any time in our sole discretion. You may reject changes by discontinuing use of the Service. Your continued use of the Service will constitute your acceptance of and agreement to such changes. Maintenance to the Service may be performed from time-to-time resulting in interrupted service, delays or errors in the Service and Comun and the Bank shall have no liability for any such interruptions, delays or errors. Attempts to provide prior notice of scheduled maintenance will be made, but Comun and Bank cannot guarantee that such notice will be provided.

Ownership and License

You agree that Comun retains all ownership and proprietary rights in the Service, associated content, technology, Mobile Banking app and website(s). Your use of the Service is subject to and conditioned upon your complete compliance with this Addendum and the Account Agreement. Without limiting the effect of the foregoing, any breach of this Agreement immediately terminates your right to use the Service. Without limiting the restriction of the foregoing, you may not use the Service (i) in any anti-competitive manner, (ii) for any purpose which would be contrary to Comun's business interest, or (iii) to Comun's actual or potential economic disadvantage in any aspect. You may use the Service only for non-business, personal use in accordance with this Addendum. You may not copy, reproduce, distribute or create derivative works from the content and agree not to reverse engineer or reverse compile any of the technology used to provide the Service.

DISCLAIMER OF WARRANTIES

YOU AGREE YOUR USE OF THE SERVICE AND ALL INFORMATION AND CONTENT (INCLUDING THAT OF THIRD PARTIES) IS AT YOUR RISK AND IS PROVIDED ON AN “AS IS” AND “AS AVAILABLE” BASIS. COMUN AND BANK DISCLAIMS ALL WARRANTIES OF ANY KIND AS TO THE USE OF THE SERVICE, WHETHER EXPRESS OR IMPLIED, INCLUDING, BUT NOT LIMITED TO THE IMPLIED WARRANTIES OF MERCHANTABILITY, FITNESS FOR A PARTICULAR PURPOSE AND NONINFRINGEMENT. COMUN AND BANK MAKES NO WARRANTY THAT (i) THE SERVICE WILL MEET YOUR REQUIREMENTS, (ii) THE SERVICE WILL BE UNINTERRUPTED, TIMELY, SECURE, OR ERROR-FREE, (iii) THE RESULTS THAT MAY BE OBTAINED FROM THE SERVICE WILL BE ACCURATE OR RELIABLE, AND (iv) ANY ERRORS IN THE SERVICE OR TECHNOLOGY WILL BE CORRECTED.

LIMITATION OF LIABILITY

YOU AGREE THAT COMUN AND BANK WILL NOT BE LIABLE FOR ANY DIRECT, INDIRECT, INCIDENTAL, SPECIAL, CONSEQUENTIAL OR EXEMPLARY DAMAGES, INCLUDING, BUT NOT LIMITED TO DAMAGES FOR LOSS OF PROFITS, GOODWILL, USE, DATA OR OTHER LOSSES RESULTING FROM THE USE OR THE INABILITY TO USE THE SERVICE INCURRED BY YOU OR ANY THIRD PARTY ARISING FROM OR RELATED TO THE USE OF, INABILITY TO USE, OR THE TERMINATION OF THE USE OF THE SERVICE, REGARDLESS OF THE FORM OF ACTION OR CLAIM (WHETHER CONTRACT, TORT, STRICT LIABILITY OR OTHERWISE), EVEN IF COMUN AND BANK HAS BEEN INFORMED OF THE POSSIBILITY THEREOF.

Geographic Constraints

You agree that you will not use the Service in locations that are prohibited under U.S. law and regulations, including laws and regulations issued by the Office of Foreign Assets Control.

Errors

You agree to notify Comun of any suspected errors regarding items deposited through the Service right away, and in no event later than 60 days after the applicable account statement is sent. Unless you notify Comun within 60 days, such statement regarding all deposits made through the Service shall be deemed correct, and you are prohibited from bringing a claim against Comun or the Bank for such alleged error.

[1] Unless it would be inconsistent to do so, words and phrases used in this Agreement should be construed so that the singular includes the plural and the plural includes the singular.

[2] You may not withdraw more than $500.00 cash at an ATM and during a POS purchase, or purchase more than $5,000 worth of goods or services on any calendar day.

[3] ACH Transactions may include, but are not limited to direct deposits, pre-authorized withdrawals, and online transfers.

[4] Business Day - Monday through Friday, except Federal holidays