Financial Education

What is a certified check and how can you make sure it’s valid?

We explain how to issue a certified check, how it differs from a cashier’s check, how much it costs, and how to verify it has funds.

8 min read

18 Dec 2025

What is a certified check and how does it work?

Certified checks are a common form of payment for thousands of immigrants living in the United States, especially for major purchases such as rent payments, buying a car, and legal settlements.

However, it is not always clear why the certification process matters and how it differs from other types of checks.

A certified check is a physical payment order that has been reviewed in advance by a financial institution to ensure there are sufficient funds in the issuer’s bank account. This is the fundamental reason it’s considered a safer form of payment than a personal check.

Below, we explain in detail what a certified check is, how it works, and why it’s important to understand the differences from other types of checks.

What is a certified check?

A certified check is a type of check with guaranteed funds, since the issuing bank has verified the money exists in the checking or personal account.

This makes it a safer form of payment than personal checks, because the bank sets aside the amount to be paid so it can be collected by the payee.

How is a certified check issued?

Issuing a certified check is a straightforward process you can complete directly at the financial institution of your choice.

- The customer requests the check

The account holder must go to a bank and request a certified check, specifying the payee and the amount.

- Customer identification

You must present an official ID to verify that you are the holder of the savings or checking account from which the funds will be drawn.

- The bank freezes the amount in the account

The bank then certifies there are sufficient funds to cover the check and freezes them to ensure the payee can cash it.

- Signature certification

You must sign the check before finishing the process so the bank can confirm the signature matches the one on file.

Affixing the certification stamp

Finally, once the bank has verified the funds and the signature, it places a certification stamp to document completion of the process.

Differences between a certified check and a cashier’s check

A cashier’s check is another way to make secure payments using a physical instrument. In this case, the bank branch issues the check after receiving the customer’s payment, so the funds come from the bank itself.

Below is a comparison between a cashier’s check and a certified check.

Cashier’s check

Certified check

Security

High; the bank verifies sufficient funds and places a hold for the payee.

Very high; the check is backed by the bank and does not depend on the issuer’s account.

Cost

At some banks they have no cost at others up to approximately $15.

Depends on the bank; typically $10–$20.

Issuance time

At the branch, after funds are verified.

Immediate.

When is a certified check typically required?

A certified check is commonly used for significant transactions or large amounts. This gives the recipient assurance that funds are available.

- Paying an apartment security deposit.

When finalizing a lease or purchasing an apartment, the landlord or agent may request payment via certified check to guarantee funds.

- Buying a used car.

Whether dealing directly with owners or dealerships, a certified check can be a suitable option because of the security it provides.

- Closing an important contract or legal settlement.

For example, to pay fees, settlements, or indemnities, certified checks provide security for both parties.

- For tuition or school fees.

Some educational institutions accept certified checks as a form of payment, especially for international or first-time payments.

Do you know what to do if a check is stolen or lost? We explain it here!

Practical tips for using certified checks safely

While certified checks are among the safest payment methods due to the bank’s verification process, there are still fraud attempts using forged documents.

With this in mind, keep these tips in mind to avoid becoming a victim of check fraud.

How to know if a check has funds and avoid scams

- Verify with the issuing bank.

Call the bank directly and provide the check number, account holder, and amount; ask them to confirm authenticity and that funds are guaranteed. Make sure you call the bank’s official number, not the one printed on the check.

- Be alert if you receive an overpayment check.

A common scam is sending a check for more than the amount due and asking for the difference in cash. Confirm the check’s validity with the bank before proceeding.

- Wait for the check to clear before handing over any goods.

Clearing can take 3–10 days. Make sure the funds have fully settled and are not just on hold.

- Avoid accepting checks from unknown parties.

Whenever possible, accept checks only from people you trust. If you must take a check, follow the security measures above.

Manage your money securely with Común

In this article we explained what a certified check is, how it’s issued, how it differs from cashier’s checks, and how to use this payment method safely.

While certified checks can be a good payment option, a checking account in the U.S. is a much more secure and practical way to manage money.

Meet Común, your financial ally in the United States!

Send, receive, and cash money within and outside the United States. Our platform lets you move your money easily, quickly, and securely. You need a qualifying official ID from your country of origin to get started.

Open your account with Común today and discover a financial platform tailored to you.

Frequently Asked Questions (FAQ)

Where can I get a certified check in the United States?

You can request certified checks at financial institutions such as banks, credit unions, and some digital banks.

How much does it cost to get a certified check at the bank?

The cost depends on the bank but is typically between $10 and $15.

What other types of checks exist in the U.S. besides certified checks?

Other types of checks in the United States include: Money order; Personal check; Cashier’s check.

About Común

Común aims to support the Latino community in the United States. It offers a debit account that can be opened with more than 100 valid Latin American IDs and an app available in Spanish.

Visit Común's website or download the app for free to learn more about the full offer and applicable terms.

Olivia Rhye

Community Partner

Financial Education

What is a certified check and how does it work?

8 min de lectura

What is a certified check and how does it work?

Certified checks are a common form of payment for thousands of immigrants living in the United States, especially for major purchases such as rent payments, buying a car, and legal settlements.

However, it is not always clear why the certification process matters and how it differs from other types of checks.

A certified check is a physical payment order that has been reviewed in advance by a financial institution to ensure there are sufficient funds in the issuer’s bank account. This is the fundamental reason it’s considered a safer form of payment than a personal check.

Below, we explain in detail what a certified check is, how it works, and why it’s important to understand the differences from other types of checks.

What is a certified check?

A certified check is a type of check with guaranteed funds, since the issuing bank has verified the money exists in the checking or personal account.

This makes it a safer form of payment than personal checks, because the bank sets aside the amount to be paid so it can be collected by the payee.

How is a certified check issued?

Issuing a certified check is a straightforward process you can complete directly at the financial institution of your choice.

- The customer requests the check

The account holder must go to a bank and request a certified check, specifying the payee and the amount.

- Customer identification

You must present an official ID to verify that you are the holder of the savings or checking account from which the funds will be drawn.

- The bank freezes the amount in the account

The bank then certifies there are sufficient funds to cover the check and freezes them to ensure the payee can cash it.

- Signature certification

You must sign the check before finishing the process so the bank can confirm the signature matches the one on file.

Affixing the certification stamp

Finally, once the bank has verified the funds and the signature, it places a certification stamp to document completion of the process.

Differences between a certified check and a cashier’s check

A cashier’s check is another way to make secure payments using a physical instrument. In this case, the bank branch issues the check after receiving the customer’s payment, so the funds come from the bank itself.

Below is a comparison between a cashier’s check and a certified check.

Cashier’s check

Certified check

Security

High; the bank verifies sufficient funds and places a hold for the payee.

Very high; the check is backed by the bank and does not depend on the issuer’s account.

Cost

At some banks they have no cost at others up to approximately $15.

Depends on the bank; typically $10–$20.

Issuance time

At the branch, after funds are verified.

Immediate.

When is a certified check typically required?

A certified check is commonly used for significant transactions or large amounts. This gives the recipient assurance that funds are available.

- Paying an apartment security deposit.

When finalizing a lease or purchasing an apartment, the landlord or agent may request payment via certified check to guarantee funds.

- Buying a used car.

Whether dealing directly with owners or dealerships, a certified check can be a suitable option because of the security it provides.

- Closing an important contract or legal settlement.

For example, to pay fees, settlements, or indemnities, certified checks provide security for both parties.

- For tuition or school fees.

Some educational institutions accept certified checks as a form of payment, especially for international or first-time payments.

Do you know what to do if a check is stolen or lost? We explain it here!

Practical tips for using certified checks safely

While certified checks are among the safest payment methods due to the bank’s verification process, there are still fraud attempts using forged documents.

With this in mind, keep these tips in mind to avoid becoming a victim of check fraud.

How to know if a check has funds and avoid scams

- Verify with the issuing bank.

Call the bank directly and provide the check number, account holder, and amount; ask them to confirm authenticity and that funds are guaranteed. Make sure you call the bank’s official number, not the one printed on the check.

- Be alert if you receive an overpayment check.

A common scam is sending a check for more than the amount due and asking for the difference in cash. Confirm the check’s validity with the bank before proceeding.

- Wait for the check to clear before handing over any goods.

Clearing can take 3–10 days. Make sure the funds have fully settled and are not just on hold.

- Avoid accepting checks from unknown parties.

Whenever possible, accept checks only from people you trust. If you must take a check, follow the security measures above.

Manage your money securely with Común

In this article we explained what a certified check is, how it’s issued, how it differs from cashier’s checks, and how to use this payment method safely.

While certified checks can be a good payment option, a checking account in the U.S. is a much more secure and practical way to manage money.

Meet Común, your financial ally in the United States!

Send, receive, and cash money within and outside the United States. Our platform lets you move your money easily, quickly, and securely. You need a qualifying official ID from your country of origin to get started.

Open your account with Común today and discover a financial platform tailored to you.

Frequently Asked Questions (FAQ)

Where can I get a certified check in the United States?

You can request certified checks at financial institutions such as banks, credit unions, and some digital banks.

How much does it cost to get a certified check at the bank?

The cost depends on the bank but is typically between $10 and $15.

What other types of checks exist in the U.S. besides certified checks?

Other types of checks in the United States include: Money order; Personal check; Cashier’s check.

Financial Education

How to Endorse a Check: Your Safe and Detailed Step-by-Step Guide

8 min de lectura

Despite the fact that digital payment methods have gained significant relevance practically worldwide, checks remain essential for carrying out certain transactions, especially for people without a banking account.

According to recent data, 61% of Americans still use checks. However, 17% have been victims of check fraud.

Knowing how to endorse a check in the United States is a necessary security measure to prevent fraud. While it can be a confusing procedure, it is crucial to understand it in order to avoid issues.

In this article, we will explain step-by-step how to correctly endorse checks, as well as the information you need to write on the back in order to cash the stated amount.

What Is a Check Endorsement and Why Is It So Important in the U.S.?

A check endorsement is a signature on the back of the check that serves as authorization for it to be cashed at a financial institution.

Its main function is to validate the cashing of the check, as well as authorize the transfer of funds, or to transfer the right to another person.

Knowing how to endorse a check is essential because it is a primary security requirement in the U.S. financial system, serving as a protection measure for the holder and the deposited funds.

What Is the Correct Way to Endorse a Check, and Where Should You Sign?

Below, we show you how to complete the endorsement before cashing checks at the bank.

Step 1: Verify the Check Details

Make sure the details on the front of the check are correct, such as the payee’s name, the amount in numbers and words, and the banking institution.

Step 2: Locate the Endorsement Area

Turn the check over and locate the statement “Endorse Here” or “Do not write below this line.” Avoid writing below the marked area.

Step 3: Sign the Check Precisely

Sign the check in the designated box, according to the type of endorsement you require. Next, we will explain everything about the different types.

But what should you do if the payee’s name is incorrect?

Example of How to Endorse a Check if the Name Is Misspelled

If the payee’s name is incorrect, you should first sign as it appears and then sign again with the corrected name.

James Smit — James Smith

Step 4: Consider a Restrictive Endorsement (Highly Recommended!)

A restrictive endorsement is a security measure to prevent an unauthorized third party from cashing the check, as it limits the form of payment to a registered banking account. It is linked to the information provided on the back of the check.

Step 5: Multiple-Payee Endorsements

If the check is made out to more than one payee, one or all may need to sign the endorsement, depending on how it is written.

- Katy Adams and Mark Palmer: Signatures from both are required

- Katy Adams or Mark Palmer: One signature is sufficient

- Katy Adams and/or Mark Palmer: Depending on the intermediary bank, one or two signatures may be required

- Katy Adams, Mark Palmer, etc.: The bank determines whether one or all signatures are necessary

Types of Endorsements: Know the Options for Your Checks

Before endorsing your check, verify which type is most suitable depending on the transaction you need to perform. For example, a restrictive endorsement is a way to secure your money, just like using modern financial alternatives such as Común, a comprehensive service that gives you access to unified and efficient financial tools.

Blank Endorsement

A blank endorsement is carried out when the same payee cashes the check in cash. In this case, only the signature in the designated area is needed.

Restrictive Endorsement

A restrictive endorsement is a security measure to ensure that the funds are deposited into a specific banking account.

To do this, you must include the statement “for deposit only to” + bank name, account number, and signature.

This is the most recommended method for Común users who make deposits via mobile, as it provides protection for the check in case of loss and ensures that the money is deposited into the designated account.

Third-Party Endorsement

If the check will be cashed by a third party, it must be endorsed as follows.

Pay to the order of: (name of another person) + signature

It is important to exercise extreme caution with this type of endorsement. Use it only with trusted individuals, and in case of theft or loss of a check, report it to the financial institution immediately.

Business Endorsement

A business endorsement is made when a check is cashed in the name of a company. This requires including the full name of the company, followed by the signature of the authorized legal representative.

Mobile Deposit Endorsement

To deposit check funds through a mobile application or mobile banking, it must be endorsed as follows:

For mobile deposit only + your signature.

Deposit your endorsed check easily and securely using Común

Cashing checks is a process that requires special care and attention in order to avoid mistakes and setbacks that could affect the transaction.

This time, we learned the importance of correctly endorsing a check in the United States, as well as the different types that exist, according to the available cashing methods.

Now that you know how to fill out a check on the back, you can rely on Común to deposit the funds through the mobile app.

Skip the lines: Deposit your check from the app; availability of funds may vary.

Común offers you the necessary security to protect your money and personal data

It is an accessible platform for immigrants in the United States; request to open your account with documentation from your country

Get customer support in English and Spanish, available 24/7

Access a comprehensive mobile app to manage your personal finances in the simplest way

Común will not only make the check deposit process easier, but it will also transform your financial life in the United States. Open your account today and find out.

Frequently Asked Questions

Is it mandatory to endorse a check in the United States?

In most cases, yes, it is necessary. If you request a deposit through an ATM or application, the bank may not require an endorsement.

What happens if I sign the check incorrectly when endorsing it?

Avoid cross-outs or scratches and endorse the check again. If the bank rejects it, ask the issuer to issue a new one.

Can I endorse a check to another person?

You can endorse a check so that it can be cashed by another person with the statement “pay to order of” along with the payee’s name. However, this process is restricted according to each bank’s specific policies.

Is it safe to deposit a check with the mobile app?

It is safe to deposit a check through the Común mobile app, as your data is encrypted and it includes other security measures such as two-step verification.

International Money Transfers

Which banks offer Zelle in Mexico? What you need to know in 2026

8 min de lectura

Which banks offer Zelle in Mexico? What you need to know in 2026

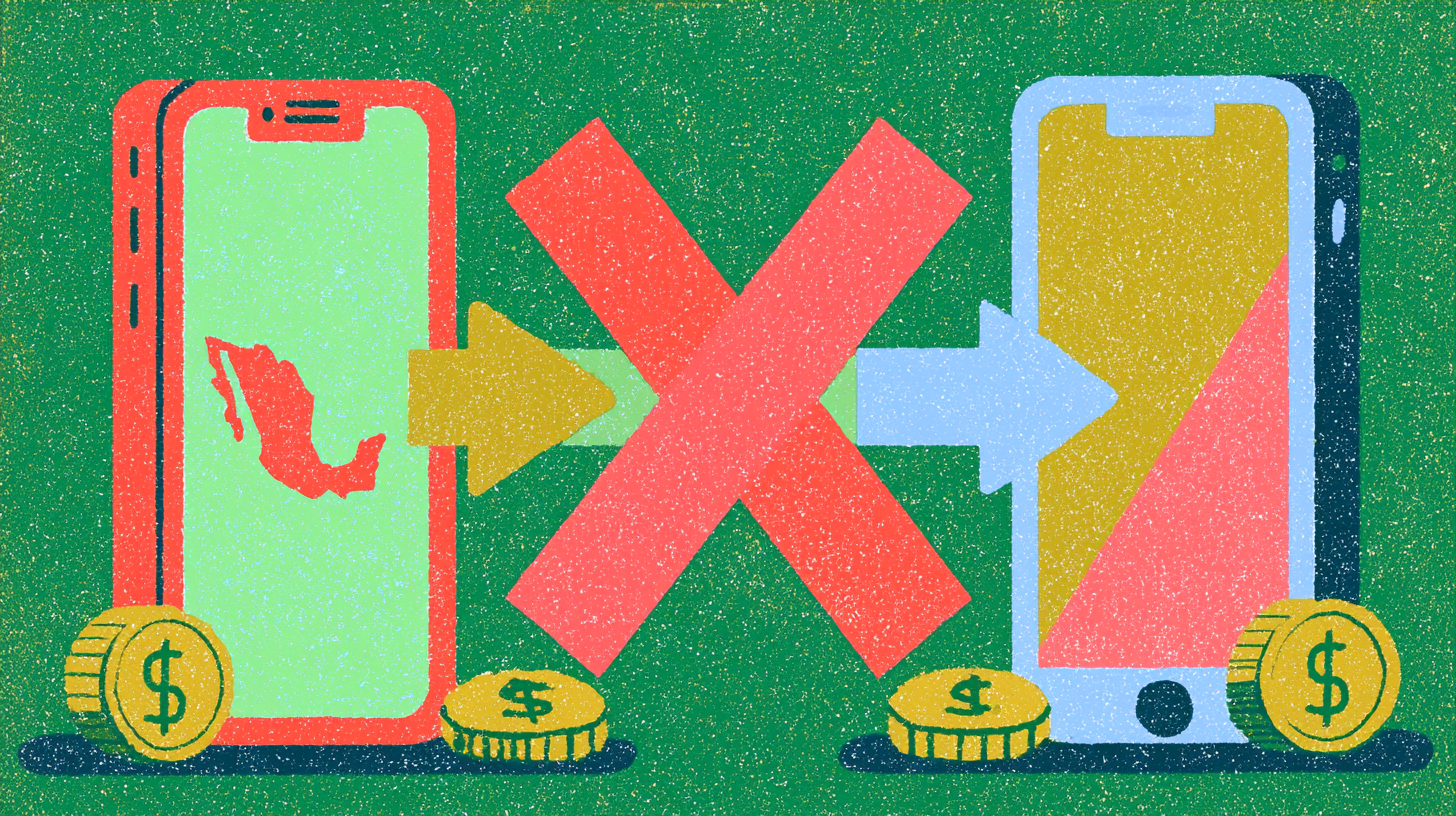

Zelle does not send money directly to Mexico. Zelle only works between eligible U.S. bank accounts and credit unions within the United States.

If you are looking into different methods for sending money to your family in Mexico, you may be searching for 'which banks offer Zelle in Mexico' or trying to understand if Zelle works internationally. This is a common misunderstanding for immigrant families in the U.S. No Mexican bank officially offers Zelle for receiving transfers from the U.S., and Zelle itself is not designed for international money transfers or currency conversion.

What is Zelle and how does it work?

Zelle is a digital payment service that facilitates peer-to-peer transfers at select partner banks in the United States. It is known for its speed, with transfers appearing in minutes, and for its extensive coverage across the U.S. Some U.S. financial institutions that support Zelle include Bank of America, Chase, Wells Fargo, Citi, PNC, and many more.

Why doesn't Zelle work for sending money to Mexico?

Cross-border money transfers require financial institutions, payment networks, regulatory approvals, identity verification procedures, and international settlement systems. Zelle was built around domestic payment systems in the U.S. Because of this, the service does not support direct transfers from U.S. bank accounts to recipients in Mexico.

Alternatives for sending money to Mexico from the U.S. (2026 comparison)

| Service | Typical starting fees | Delivery speed | Exchange rate model | Cash pickup |

|---|---|---|---|---|

| Remitly | Varies; ~$1.99+ for bank deposit to Mexico | Express: minutes to same day; Economy: 3–5 days | Exchange rate markup applies | Yes |

| Wise | From ~0.48% of transfer; shown upfront | Usually same day to 2 days | Mid-market rate, no markup | Limited (select corridors) |

| Xoom | Depends on payment method and destination | Minutes to 1 day | Exchange rate markup applies | Yes |

| Western Union | Varies widely by method and destination | Minutes to several days | Exchange rate markup applies | Yes (extensive agent network) |

| Común | Starts at $2.99 via UniTeller; may vary | Varies by destination and method | Rates displayed before transfer | Yes (depending on delivery option) |

Fees, exchange rates, and delivery times vary based on transfer amount, destination, funding method, and payout option. In 2026, a 1% federal excise tax applies to cash-funded transfers. Bank, debit, and credit card transfers are exempt.

How the new 1% tax on cash remittances affects transfers to Mexico

Starting in 2026, a 1% federal tax applies to certain remittance transfers. The tax applies when you pay with cash, money order, or cashier's check. Transfers funded from a U.S. bank account or with a U.S.-issued debit or credit card are exempt by law.

FAQ

Does Zelle work in Mexico?

No. Zelle does not support international transfers. There is no Mexican bank that offers Zelle for receiving money from the U.S.

What is the best app to send money to Mexico?

It depends on your specific situation. Común offers transfers starting at $2.99 with transparent pricing. Visit comun.app/remittances to learn more.

Remittance service provided by Service UniTeller, Inc. Remittance fees start at $2.99 but may vary. Común Inc. may earn revenue from the conversion of foreign currencies.

.png)

Financial Education

What is a W-2 form? Complete 2026 guide for immigrant workers in the U.S.

8 min de lectura

What is a W-2 form? Complete 2026 guide for immigrant workers in the U.S.

A W-2 form is one of the most important tax documents employees receive in the United States. If you worked for an employer during the year, your W-2 shows how much money you earned and how much money was withheld for taxes.

For many immigrant workers, this may also be the first time dealing with U.S. tax documents. Understanding how to read a W-2, when you should receive it, and what to do if something is incorrect can help you file taxes more confidently and avoid delays during tax season.

This article is for informational purposes only and does not constitute legal or tax advice. It is recommended to consult a qualified tax professional for guidance specific to your situation.

What is a W-2 form?

A W-2 form, officially called the Wage and Tax Statement, is a tax document employers send to employees every year. The form reports: total wages earned, federal income taxes withheld, Social Security and Medicare taxes withheld, state or local tax withholdings if applicable.

The IRS requires employers to provide a W-2 to employees who earned wages during the tax year. You typically receive a W-2 if you are considered an employee of a company. Independent contractors and certain gig workers generally receive Form 1099 rather than a W-2.

When should you receive your W-2?

Employers must send W-2 forms to employees by January 31 of the year following the reported tax year. If you haven't received your W-2 by early February, contact your employer. If you still don't receive it, you can contact the IRS for assistance.

What information does the W-2 contain?

- Box 1: Wages, tips, and other compensation

- Box 2: Federal income tax withheld

- Box 3: Social Security wages

- Box 4: Social Security tax withheld

- Box 5: Medicare wages

- Box 6: Medicare tax withheld

- Boxes 15–17: State tax information

W-2 vs. 1099: what is the difference?

| W-2 employee | 1099 contractor |

|---|---|

| Employer withholds taxes | Worker usually pays taxes independently |

| May receive benefits | Usually no employer benefits |

| Employer generally has greater control over work duties | Worker has more independence |

| Receives W-2 in January | Receives 1099-NEC if eligible |

Can ITIN holders get a W-2?

Yes. Employees can receive a W-2 using an ITIN instead of an SSN. If you are legally working in the U.S. with work authorization but do not yet have an SSN, you can use your ITIN for tax purposes. However, remember that an ITIN does not authorize employment on its own. For more information about ITINs, visit comun.app/itin.

What to do if your W-2 has errors?

If you find errors on your W-2, such as an incorrect name, SSN/ITIN, or incorrect figures: contact your employer immediately to request a corrected W-2 (Form W-2c), wait for the corrected W-2 before filing your tax return, if you cannot get a correct W-2 in time, the IRS has procedures to help you.

FAQ

What is the W-2 form?

It is the Wage and Tax Statement your employer sends you each January, showing how much you earned and how much you paid in taxes the previous year.

When will I receive my W-2?

No later than January 31 of the year following the reported tax year.

What do I do if I don't receive my W-2?

First contact your employer. If unresolved, you can contact the IRS for assistance.

This article is for informational purposes only and does not constitute legal or tax advice. Común is a financial technology company and not a bank. Banking services are provided by Community Federal Savings Bank, Member FDIC.

International Money Transfers

How much does it cost to send money to Mexico from the United States? A 2026 guide

8 min de lectura

How much does it cost to send money to Mexico from the United States? A 2026 guide

In most cases, the total cost depends on three factors: the transfer fee, the exchange rate, and any charges applied to the recipient of the money. The truth is that the final cost can range from a few dollars to something more significant as it is impacted by the service fee, delivery method, and speed.

Remittances have become so important to the Mexican economy that Mexico remains the world's second-largest recipient of remittances, behind only India. According to BBVA Research, Mexico received $61.8 billion USD in remittances in 2025, representing 3.4% of the country's GDP. Today, there are dozens of apps and money transfer services available for sending money from the United States to Mexico. Some focus on speed, others on cash pickup access, and some prioritize lower overall costs.

In this guide, we'll break down what actually affects the cost of a transfer, compare popular services, and explain how to find the option that works best for you and your family.

How much money can I send to Mexico?

One very important aspect to consider is the amount allowed by money transfer apps, as well as any restrictions included in their terms and conditions.

In general, there is no legal limit imposed by the United States government, but each platform has its own standards and regulations that determine transfer limits and guidelines for international money transfers.

For example, these are some of well known providers that offer money transfers to Mexico and their respective limits:

- Western Union: up to 5,000 USD per transaction.

- MoneyGram: up to 10,000 USD per transaction.

- Xoom: Level 1 is limited to $2,999 per day while the third level allows up to $50,000 per day.

If you are looking for a straightforward way to send money to Mexico, Común can be an excellent alternative. New users can enjoy the first money transfer free and then pay a fee starting at 2.99 USD per transfer, up to applicable limits.

What is the best way to send money from the United States to Mexico?

There are several ways to send money from the United States to Mexico, whether through traditional banks or specialized international money transfer services. These are the main options to do it:

Bank-to-Bank transfers

One of the most common ways to send money is through wire transfers from one traditional bank to another. The advantage of this method is that it can be secure because it is backed by official financial institutions. However, transfers can take longer and involve higher fees.

To send funds this way, you must have a U.S. bank account and use the recipient's SWIFT code.

The transfer cost depends on the receiving bank in Mexico. For example:

- BBVA charges approximately $30 USD + VAT to receive an incoming international transfer.

- Citibanamex estimates suggest around $15–20 USD + VAT for incoming transfers, but confirming directly with the bank is recommended.

These fees apply regardless of the amount sent, therefore it is important to confirm the fees with each bank.

Cash transfers

Another option, which may be more accessible for people without a bank account, is sending cash that can be picked up at different locations across Mexico.

To send cash, it is common to visit a physical location of the provider that offers this service, such as a Western Union office. Once there, you pay the amount you want to send plus the assigned fee. To collect the funds, your family members must present a valid government ID at one of the participating locations, such as Oxxo, Banco Azteca, Walmart, or others. However, many service providers such as Western Union also have digital offers.

Although this can be a convenient alternative for people who mainly manage cash, it may also come with potential drawbacks, such as fees that vary depending on the amount sent and exchange rates that might be less competitive compared to some digital transfer services.

Apps and digital platforms

Another option for sending money to Mexico is through apps and digital platforms that specialize in international money transfers, such as Wise, Félix Pago, Ria Money Transfer, and Común. Many of these services are available on both iOS and Android and may offer lower costs compared to some cash transfers or traditional bank wires, depending on the provider and delivery method. Some platforms focus mainly on money transfers, while others may also include additional financial features, such as a debit card or access to a U.S. bank account.

To access these services, you must create an account on the provider's website or app. In addition, some apps require identity verification using personal information such as your SSN (Social Security Number) or ITIN.

You can send money directly through the provider's app or, in some cases, even through WhatsApp, and choose the preferred delivery method. Some services also offer cash pickup options for recipients. For example, Común accepts more than 100 Latin American IDs for account verification, it allows you to send money through the app or via WhatsApp, and offers cash pickup options across Mexico.

Before choosing an app to send money to Mexico, we recommend comparing the most popular options and evaluating which one best fits your needs and those of your family.

Five popular mobile apps for sending money to Mexico from the United States

There are many apps available for sending money from the United States to Mexico, but costs, delivery speeds, and exchange rates can vary depending on the provider and transfer method. Comparing multiple options can help you find the service that best fits your needs.

| Service | Payment Options | Fee | Delivery Options | Exchange Rate | MXN per 1,000 USD | Speed |

|---|---|---|---|---|---|---|

| Común | Bank account, debit card, cash | Starting at 2.99 USD | Bank account or cash pickup | Competitive | ~17,000 MXN | Minutes to hours |

| Western Union | Bank, cash, card | Varies depending on amount | Bank, cash, wallet | Exchange rate with spread applied | ~16,920 MXN | Minutes to days |

| Félix Pago | WhatsApp, cash, card | $2.99 USD for bank account and $4.98 USD for cash pickup transfers | Bank account and cash | Competitive | ~17,000 MXN | Instant |

| Ria Money Transfer | Bank account (ACH), debit card, credit card, cash | Starting at $0.99; free for bank transfers up to $15,000 | Bank account, cash pickup, mobile wallet | Exchange rate with spread applied | ~16,900–17,000 MXN | Minutes to days |

| MoneyGram | Bank account, debit card, credit card, cash (at agent) | Free for bank transfers up to $10,000; $49.99 for $10,001–$15,000; $5+ for cash sends | Bank account, debit card, mobile wallet, cash pickup | Exchange rate with spread applied | ~16,800–16,950 MXN | Minutes to hours |

The amount received in MXN for every 1,000 USD can change throughout the day due to fluctuations in exchange rates, provider fees, and delivery methods. The rates shown here are for illustrative purposes only and may not reflect the exact amount available at the time of your transfer. Before sending money, it may be helpful to compare the current exchange rate and total transfer cost across providers. Común's comparison tool can help you check and compare available rates in real time.

What determines the real cost of sending money to Mexico?

When comparing money transfer services, many people focus only on the advertised transfer fee. But the real cost of sending money to Mexico usually depends on three different factors:

- The transfer fee.

- The exchange rate spread.

- Charges applied to the recipient.

Understanding these costs can help you compare services more accurately and avoid situations where your family receives less money than expected.

Transfer Fee

The transfer fee is the most visible cost. This is the amount the provider charges to process the transaction.

Some services charge a flat fee per transfer, while others adjust the fee depending on the amount sent, the payment method, or how quickly you want the money delivered. In some cases, companies may offer promotional pricing or even a free first transfer for eligible users.

Although low fees can help reduce costs, they may not always result in the lowest overall transfer cost once exchange rates and other charges are taken into account.

Exchange rate spread

The exchange rate spread is one of the most important and often least visible parts of the total cost.

Some service providers do not use the exact market exchange rate you find on Google or financial websites. Instead, they add a margin, also known as a "spread," when converting USD to MXN.

This means that even a small difference in the exchange rate can significantly reduce the amount your recipient receives in pesos, especially on larger transfers.

A service with a slightly higher transfer fee but a more competitive exchange rate may actually deliver more money to your family in Mexico.

Recipient charges or withdrawal costs

In some cases, additional costs may appear after the transfer is sent. Depending on the provider and delivery method, the recipient could face charges for cash pickup, ATM withdrawals, bank processing, or currency conversion. Some banks and pickup locations may also apply their own service fees.

These extra costs are important because they directly affect the final amount your recipient can actually use.

Compare the full cost

The best way to compare money transfer services is to look at the total outcome: how much you pay, how much your recipient receives, and how long the transfer takes.

If possible, it is recommended that before sending money, you review the transfer fee, compare the exchange rate, and check whether there are any recipient-side charges. Small differences across these three factors can add up quickly over time.

To compare real-time transfer costs, exchange rates, and delivery options, you can use tools like Común's compara before making your transfer.

How can I send money to Mexico with Común?

With Común you can send money to your family and friends in Mexico directly from Común's mobile app without leaving your home.

You can follow these steps:

- Open your Común mobile app.

- On the main page, select "Send a Remittance."

- Select the recipient you want to send the international transfer to.

- You can register a recipient using their banking details, including full name, bank name, and phone number.

- After registering the recipient, enter the amount you want to send and review the transaction costs.

- Confirm the details and select "Confirm International Transfer."

- The recipient should receive the money within minutes. If you select a store pickup, the person can collect the money about 30 minutes after confirming the transaction.

- You can check the transfer status in your Común mobile app by clicking on the transaction.

Transfer fees start at 2.99 USD per transaction, up to applicable limits.

Send money to Mexico easily and securely

Today, there are more options than ever for sending money from the United States to Mexico. Whether you prefer the familiarity of a traditional bank, the convenience of cash pickup, or the flexibility of a digital platform, the right choice will depend on your own situation.

Comparing fees, exchange rates, delivery methods, and transfer times may help you find an option that better fits your needs and the way your family prefers to receive money.

With Común you can open an account using more than 100 Latin American IDs, send money from the comfort of your phone and access multiple delivery methods across Mexico.

Living in the United States

Discover how much it costs to live in the United States

8 min de lectura

Knowing the cost of living in the United States is essential if you plan to build a life in this country. It includes the amount of money needed to cover basic expenses such as housing, food, health, public transportation, etc.

You’ve surely asked yourself before how much money you need to live well in the U.S. The reality is that this figure is relative, since costs vary considerably from one State to another.

However, in general terms, it is possible to state that the main expense is housing, followed by food and health services.

This time, we will explain how much it costs per month to live in the United States, which is the cheapest State to live in the USA, and the approximate costs you will have to cover so you can consider your monthly budget.

What does the cost of living in the United States mean?

Cost of living refers to the amount of money required to cover the necessary expenses to subsist, which are divided as follows:

- Housing: monthly rent or mortgage.

- Food: purchasing groceries and prepared food.

- Transportation: public transit or your own car.

- Health: health insurance, medical care, medications, treatments, etc.

- Education: tuition, school supplies.

- Basic services: electricity, water, internet.

The average cost of living varies in each State, because each one has a particular lifestyle that may be more or less affluent, depending on the type of services available and the area’s infrastructure.

Knowing which States are the cheapest in the United States is essential to adjust your monthly expenses in a competitive way.

Main expenses in the United States

Starting a new life in the United States entails covering a series of monthly expenses that could affect your finances if they are not planned correctly.

Below, we show you the national average of basic necessities in this country.

Housing: the largest monthly expense

Housing is the largest expense you will have once you arrive in the United States, especially if you plan to live in a city like New York, known for its high costs.

Housing costs also depend on whether it is a mortgage or rent.

In March 2025, the average rent was $1.575 USD for a one-bedroom apartment and $1.835 USD for a two-bedroom apartment.

On the other hand, in the same month, the average mortgage rose to $2.807 USD, which represents an increase of 5.3%.

Food and basic services

According to the Thrifty Food Plan from the United States Department of Agriculture (USDA), an adult between 20 and 50 years old requires approximately $309.20 USD per month, while a child between 9 and 11 years old spends around $234.20 USD.

Health and health insurance

As for health insurance, the cost depends on several factors, such as the beneficiary’s age, place of residence, and level of coverage.

This is the national average cost by level of coverage for people over 40 years old.

- Bronze: $488 USD

- Silver: $621 USD

- Gold: $676 USD

- Platinum: $913 USD

Transportation: public vs. own car

For its part, the national average cost of public transportation in the United States reaches $975 USD annually or $81 USD monthly, while the cost of maintaining a car exceeds a thousand dollars per month.

Cost of living in the United States by State and city

Remember that the previous figures are a nationwide average, so prices may be lower or higher depending on the city and State where you intend to live.

| City / State | Cost of living index1 | Average monthly salary2 | Income needed for a single person3 | Income needed for a family of 4 (2 adults and 2 children)4 |

|---|---|---|---|---|

| San Francisco, California | 67% higher than the national average | $7,938 | $9,993.16 | $28,260 |

| New York | 74% higher than the national average | $4,331.58 | $11,547 | $26,533 |

| Washington, D.C. | 42% higher than the national average | $6,658 | $9,138 | $23,157 |

| Miami, Florida | 21% higher than the national average | $5,153 | $9,083.45 | $22,707 |

| Boston, Massachusetts | 46% higher than the national average | $6,750 | $10,413 | $26,663 |

| Austin, Texas | 3% lower than the national average | $5,419 | $8,313 | $19,1665 |

¹ RentCafe, 2025

² ZipRecruiter, 2025

³ Smart Assets, 2024

⁴ Smart Assets, 2025

⁵ Click2Houston, 2025

As you can see, the cities of New York and San Francisco are among the most expensive nationwide, so it is advisable to choose a more accessible place to live, such as Texas.

Remember that these data are an estimate and your salary could be higher or lower, as could your monthly expenses and the money needed to live.

What is the average salary in the United States?

Another important aspect in determining the cost of living in the United States is the average salary and the minimum wage—concepts that could be confused but are actually very different.

On the one hand, the minimum wage is the amount from which an employer must start to set employees’ pay. It is established by law.

This varies in each State. According to the U.S. government, at the federal level this figure reaches $7.25 USD per hour, although several States set a higher minimum. For example, in California and New York it is $16.50 USD.

The average salary is the average income a worker receives per month. This amount is obtained by adding total wages and dividing by the number of workers.

By contrast, the real amount needed to live comfortably is the sum of the average costs of essential services such as housing, utilities, and food, in addition to other types of expenses such as leisure.

It is very important to be clear about the difference between the average salary and the real cost of living, since it is likely that your salary will not match your needs, especially if you are the head of a large family.

For example, while the average salary in San Francisco, California, is $7,938 USD, the amount needed to live is $9,993. In contrast, it is worth highlighting States such as West Virginia, where the average salary is $5,405 per month and the income needed to live is $6,735 USD. As you can see, the gap is much smaller, which places this State as the most accessible to live in the United States.

Manage your money better in the U.S. with Comun

Having a checking account will make financial control easier so you can stay on top of all your monthly expenses, organize income, and send money home.

That’s what Comun is for! A financial platform designed for day-to-day needs in the United States through an easy-to-use mobile app that is available in English and Spanish. Opening an account is very easy and fast; you can do it with qualifying official identification from your country of origin.

In addition, it makes it easier to send remittances to several countries, up to the applicable limits, without complications, so that your family receives more money for less.

Why choose Comun?

- Get a Visa debit card.

- Send money home with accessible, transparent fees.

- Save money and pay your bills easily.

- Anti-fraud security

And much more!

Open your account with Comun today and manage your financial life in the United States with security and confidence.

Frequently Asked Questions (FAQ)

Which city in the United States is the cheapest?

Within West Virginia, cities such as Huntington, Charleston, or Parkersburg are often among the most affordable in the country.

Which state in the USA is more affordable to live in, according to the cost of living?

West Virginia is considered an affordable State in the country.

How can I calculate the monthly cost according to my lifestyle?

Add up your necessary monthly living expenses, for example:

Monthly cost: Housing+Utilities+Food+Transportation+Other

Living in the United States

Step by step: how to file taxes for the first time as an immigrant in the U.S.

8 min de lectura

Basic requirements to file taxes for the first time in the United States

Although getting a job in the United States brings a series of benefits for the quality of life of immigrants and their families, it also means committing to fulfilling the obligations required by the country's laws.

Filing a tax return is one of the processes everyone who has earned income must complete. This is done by submitting a report of annual income to the Internal Revenue Service (IRS).

Filing a tax return is particularly important for everyone, as it opens the door to access financial services such as mortgage and personal loans, which in turn help build a financial record especially for immigrants.

Filing taxes is a stressful and often confusing process for most people, especially when it involves understanding the tax institutions of another country.

Below, we show you a step-by-step guide to help you fulfill your tax obligations in the U.S. and access the benefits that come with it, such as receiving refunds and building a financial record in the country.

What documents do you need to file your taxes?

The first thing you should know to file your tax return in the U.S. is the documentation required by the IRS to process your information.

Make sure you have the following documents:

- Tax Identification Number: if you do not have a Social Security Number (SSN), you must apply for an Individual Taxpayer Identification Number (ITIN).

- Qualifying official identification from your home country: valid passport, driver’s license, or any official document that verifies your identity.

- Proof of income: W-2 forms if you are a salaried employee and your employer withholds taxes, and Form 1099 if you are self-employed.

- Proof of address in the United States: utility bill or rental agreement.

- Financial information: checking account and routing number to receive your refund through direct deposit, if any.

Tax preparation: step by step for your first filing

It is important to stay alert during tax season and prepare in advance to meet the deadlines established by law.

Follow these steps to ease the stress of tax obligations.

Step 1. Gather all your documents

The first step is to gather all the necessary documents to file your annual tax return.

- Form W-2: this document details your salary and the amount of taxes already withheld; request it directly from your employer.

- Form 1099: used by people who work independently.

- Benefit or assistance letters: if you receive any government benefit or tax credit, the IRS sends letters to include in your tax return.

Step 2. Choose how to file

Once you have your documentation in order, you must decide how you will file your return: on your own or with professional help.

- Self-prepared tax filing: you can use various IRS-approved tax preparation software such as IRS Free File, TaxSlayer, or TurboTax, which simplify the process by automatically calculating your taxes.

- With the help of a tax preparer, if you have multiple income sources or are self-employed, the best option is to hire an authorized preparer to ensure everything is filed correctly. You can also go to a community organization that offers low-cost assistance.

Step 3. File your tax return in the United States on time

Keep in mind that the deadline to file your tax return is usually April 15 each year. It is essential to submit your tax return within the deadline to avoid penalties and delays in receiving your refund.

How much does it cost to file taxes, and which option is best for you?

As mentioned before, there are different ways to file your tax return, which vary in cost and level of support offered. The best option depends on several factors, such as your income level and how familiar you are with tax topics.

Below is a comparative table of the different ways to file taxes in the United States.

Method

Approximate cost

Level of support

Doing it yourself with IRS-approved software

Free or up to $25

Low. Although the platform guides you step by step, you must enter all the information yourself.

With the support of community organizations

Free or up to $50

Medium. You receive assistance from certified volunteers.

With private preparers or accountants

$150 to $500, depending on complexity

High. The preparer does all the work and answers your questions.

Practical tips to avoid mistakes in your first tax filing

If this is your first time filing taxes in the United States, it may seem like a very complex task. Keep these tips in mind to ease the stress associated with the process.

- Don’t wait until the last minute to file: keep the deadline in mind and prepare several weeks in advance.

- Verify that all forms match your income: remember that the required form depends on your type of work. Make sure your income matches what you report.

- Keep copies of all submitted documents: create both a physical and digital file to have every record handy.

- Check official IRS resources for immigrants: always access official websites ending in .gov.

- Avoid relying on third parties that promise higher refunds: remember that tax preparers or community organizations must be certified by the IRS to ensure your filing is done properly and your personal data remains secure.

Común, your financial support after filing your taxes

We’ve shown that the tax filing process is not as complicated as it seems. Now you know which steps to take and which method to use based on your situation.

Just as filing taxes helps you organize your financial situation, Común helps you manage your day-to-day finances.

Discover all the benefits of Común!

- Open a checking account with a qualifying official identification from your home country.

- Mobile app available in Spanish and English, specially designed for the immigrant community.

- Ability to receive your tax refund directly into your account.

- Debit card for daily expenses and international money transfers to Latin America.

Discover Común, the option dedicated to serving the needs of immigrant communities in the United States, with support available in Spanish.

Frequently Asked Questions (FAQ)

If you still have questions, check this section.

What happens if I don’t file my taxes in the U.S.?

Not filing your tax return may result in IRS penalties, accumulated interest, and withheld future refunds.

Can I file taxes without a Social Security Number?

If you do not have a Social Security Number, you can apply for an ITIN.

Is it better to file my taxes myself or with a tax preparer?

It depends on your situation: if you have only one source of income, you can use software, but if your income is higher or more complex, the best option is to consult a professional.

Living in the United States

Best Free Online English Courses for Immigrants in the U.S.

8 min de lectura

Some of the best English classes to learn online as an immigrant in the U.S.

Although moving to the United States brings a number of benefits due to the wide range of job opportunities available, it also presents challenges, such as the language barrier, which can limit opportunities for many immigrants who have not had access to formal language education.

While it may seem like a difficult goal to achieve, speaking English can make many aspects of daily life easier — such as getting a job, going to school, or handling important paperwork.

Fortunately, technology allows more people to learn English for free and easily, through platforms and mobile apps that offer lessons from anywhere. Below, we’ll show you some of the best options for immigrants who live or plan to live in the United States to learn English.

5 Reliable Platforms to Learn English from Scratch

For many people, taking in-person English classes isn’t always the best option due to cost, schedules, and transportation challenges. If you face any of these obstacles, you should know about practical alternatives from educational institutions and online platforms — ideal for those who prefer a more academic or progressive learning path.

Below, we present 5 reliable alternatives for learning English online.

British Council

This is one of the most prestigious English teaching institutions worldwide. Its platform offers a variety of courses for beginner, intermediate, and advanced students, segmented by skills: listening comprehension, grammar, writing, and conversation.

It stands out as a very complete option since students can supplement lessons with various materials such as podcasts, videos, and exercises prepared by certified English teachers.

Coursera

Coursera is a platform that offers free English courses in collaboration with prestigious universities, maintaining an academic and professional focus.

This is an excellent option if you’re looking to improve your English to access better job opportunities or refine specific skills to sound more like a native speaker.

BBC Learning English

This platform focuses on teaching English through current content, such as international and cultural news. It’s an ideal alternative for students who want to improve listening comprehension and expand their vocabulary.

USA Learns

This is an official U.S. government platform. It is specifically designed for people who want to acquire basic language skills to handle real-life situations such as visiting the doctor, ordering food, or completing immigration paperwork.

Alison

Alison is another dynamic alternative that offers a variety of free courses across different levels and practical skills. Students can also focus on specific areas, such as business English or preparation for certifications like the TOEFL.

Platform

Type of Course

Level

Main Benefit

British Council

Courses segmented by skills, general English.

From beginner to advanced.

Structured learning units with rich study materials.

Coursera

Academic and professional English.

From intermediate to advanced.

Courses focused on improving professional communication skills.

BBC Learning English

Everyday English.

From beginner to advanced.

Short lessons based on current topics.

USA Learns

Practical English.

Beginner.

Designed to equip students with the skills needed to communicate in everyday situations.

Alison

Business English and official certification preparation.

From beginner to advanced.

Offers the option to earn official digital certificates.

Mobile Applications to Learn English for Free

In addition to the options above, you can also explore other alternatives known for their flexibility in helping you learn English easily.

Mobile language-learning apps let users study anywhere, anytime, and serve as a fun complement to traditional courses.

Duolingo

Duolingo is the most famous and culturally influential app. It uses gamified lessons that unlock progressively as users acquire new skills. It’s ideal for building vocabulary.

Mondly

Mondly focuses on conversational practice and pronunciation using tools like voice recognition and artificial intelligence to interact with virtual characters.

Busuu

Busuu is one of the most comprehensive language-learning apps. In addition to structured lessons based on the Common European Framework, it allows students to interact with native speakers.

Memrise

Memrise focuses on improving listening comprehension and learning new vocabulary through videos of real-life situations presented by native English speakers.

HelloTalk

HelloTalk makes English practice easier by connecting people around the world interested in cultural and language exchange.

How to Choose the Right English Course for You

As you can see, there are many ways to learn and improve your English. Each has different approaches and benefits, so there’s no single “best option” — it depends on your level and specific needs.

Before deciding which online English course is best for you, consider these recommendations:

- Define your goals: be clear about why you want to learn or improve your English.

- Evaluate your current English level: whether you’re a beginner or already advanced.

- Compare platforms and apps: take time to find the one that best fits your needs.

- Review the course duration and format: make sure to organize your time so you can attend classes consistently and on schedule.

- Complement your study with conversation practice: it’s very important to engage with native speakers in real-life situations and different accents.

The most important factor in making language study effective is consistency, regardless of which platform you choose.

Practical Tips to Improve Your English Every Day

In addition to the classes on platforms or the interactive resources in apps, it’s important to incorporate strategies that help improve your confidence and fluency when communicating in English.

Here are some practical tips designed to make life easier for immigrants in the United States.

- Listen to English every day: whether on YouTube videos or movies. The goal isn’t to understand 100%, but to start getting used to the language.

- Practice with friends or coworkers: if you have people you trust, don’t hesitate to ask them for help.

- Apply what you’ve learned in your environment: mentally review your surroundings and try to name the things around you in English.

- Use technology to your advantage: rely on AI-powered tutors or platforms that offer automatic corrections.

Learning English and managing your finances with Comun are key steps to achieving your goals in the U.S.

In this article, we explained why learning English is important if you plan to live in the U.S., and showed you various platforms and apps designed to help you build essential language skills.

Fortunately, the immigrant community in the U.S. has allies dedicated to supporting them through their adaptation and growth in the country.

Discover Comun — the digital platform designed to meet the financial needs of immigrants.

At Comun, we believe every new learning step brings you closer to your dreams: learning English and organizing your money with Comun are steps toward achieving your goals in the United States.

Frequently Asked Questions (FAQ)

What is the best free online English course for beginners?

There are several English course options. If you have no prior knowledge, it’s recommended to start with British Council courses and complement with Duolingo.

How long does it take to learn basic English?

It depends on your consistency. If you dedicate even a small amount of time daily, you should notice improvement within three months.

What’s the best free method for adults to learn English?

There isn’t just one method to learn English. Try combining practice across different language skills using interactive platforms.

Living in the United States

How to Get a Driver’s License in the United States as a Foreign National

8 min de lectura

Driver’s license in the United States for foreign nationals: steps and requirements

Having a driver’s license makes everyday tasks easier, such as going to work, the supermarket, school, medical appointments, and more. This process is especially important for immigrants living in the United States, as it gives them independence and stability in the country.

Although the process to obtain a driver’s license varies in each state, foreign nationals do have the possibility and the right to obtain one. Below, we explain all the details so you can get this permit soon.

Can you drive with an international license in the United States?

If you have recently arrived in the United States and need to get around in your own car, you may temporarily use the driver’s license from your home country, as long as it is issued in English or accompanied by an international driving permit.

As a new driver in the United States, you must understand the difference between an international license and a local one: the former supplements your national license and allows you to drive in the U.S. for a few months; the latter is issued by the Department of Motor Vehicles (DMV) in each state and grants you a permanent permit to operate a motor vehicle in the country.

Regulations differ in each state: for example, in California you can drive with a valid foreign license until you become a resident. In contrast, in Texas your national license is valid for 90 days, and you must always carry your passport or visa.

Allowed period to drive with a foreign license

The maximum time allowed to drive with a foreign license varies depending on each state’s local regulations. In general, the period can range from 30 days to one year, from the day you arrive until you establish yourself as a permanent resident.

When is it necessary to apply for a U.S. driver’s license?

If you plan to live in the United States for a longer period, you need a U.S. driver’s license to drive. It is also essential if you plan to buy a car.

Also, remember that in some states the period to drive with a foreign license is limited, so you should consider applying for a U.S. license before that deadline expires.

Requirements to obtain a driver’s license in the U.S. as a foreign national

The requirements to obtain a driver’s license also vary by state, although the general structure is similar.

This is the documentation needed to obtain a driving permit in the United States.

- Valid passport or official identification: used as proof of identity.

- Proof of residency: can be a utility bill, rental agreement, or official letter showing your address.

- Immigration status or proof of legal presence: such as the Employment Authorization Document (EAD) or the I-20 form for students.

- Social Security Number (SSN) or an SSA ineligibility letter.

Keep in mind that states such as New York and Illinois allow applicants to obtain a driver’s license without considering immigration status.

Learn here how to send money without a bank account.

5 steps to apply for your U.S. driver’s license

Getting your driver’s license may seem like a complex and tedious process. In reality, you only need to stay organized and take the time to understand the guidelines.

Step 1. Gather your documents

Before going to a DMV office, make sure to prepare the required documents. In the previous section we outlined what you generally need, but remember to check for variations in the state where you live.

Step 2. Schedule an appointment at the DMV

Then, visit the DMV website and book an appointment. On the scheduled day, your documents will be reviewed and you will be given a date for the written exam.

Step 3. Take the written exam

The written exam evaluates your knowledge of traffic rules and road safety. Each state offers a driver’s manual to study for the test, and some are available in other languages, such as Spanish.

If you pass, you will receive a learner’s permit that will allow you to take the driving test under the guidance of an instructor.

Step 4. Take the driving test

The next step is probably the most challenging, as you must apply your theoretical knowledge in real driving practice. During the test, the instructor will evaluate your ability to follow traffic signs, park, turn, and follow safety rules.

Step 5. Pay the corresponding fees

Once you pass your driving test, you must pay a fee that varies by state. Initially, you will receive a temporary license and later receive your permanent license by mail.

Costs, timelines, and validity of a U.S. driver’s license

The cost of a driver’s license in the United States depends on each state, but generally includes the cost of the written exam, driving test, and issuance. The validity also varies by state, but it is usually between 4 and 8 years.

Additionally, a positive update for immigrants is that more states are removing immigration status requirements to issue a driver’s license; this is the case in California, New York, and Illinois.

If you have questions about the specific requirements in your state, check the updates on the official DMV website.

Drive toward your financial independence with Comun

Having a U.S. driver’s license represents another step toward achieving financial independence and making it easier to move around your city. Therefore, it is essential to understand the process to obtain one, as well as the differences in each state.

In other words, having a license simplifies and improves your life by making everyday tasks more accessible. Likewise, Comun is the financial platform that helps you manage your money safely and without complications.

Open your account with Comun and take the next step toward your independence in the United States. Manage your money with confidence, clarity, and support at every step.

Frequently Asked Questions (FAQ)

If you still have questions, check the following section.

How long can I drive with my foreign license in the U.S.?

The duration varies depending on the state you are in, but generally ranges from three months to one year.

What happens if my immigration status changes after I obtain my license?

If your immigration status changes after you obtain your driver’s license, it is recommended to update your information at the DMV. You may need to apply for a new license or present updated immigration documentation.

Is it valid to use an international license in all states?

Although the international driving permit (IDP) is accepted in most states, it must be accompanied by a valid national license. Additionally, there may be restrictions on how long it can be used in each state.

Can I get a driver’s license without a Social Security Number (SSN)?

Yes, it is possible to apply for a driver’s license without an SSN in several states. In this case, you must present an ineligibility letter issued by the Social Security Administration (SSA).

Checking account

Los Pros y Contras de Usar Cheques en los Bancos De Estados Unidos

8 min de lectura

Cobrar un Cheque en tu Propio Banco

Cuando se trata de cobrar un cheque, una de las opciones más sencillas es visitar tu propio banco o institución financiera. Aquí tienes un proceso paso a paso para depositar o cobrar un cheque:

- Endosa el Cheque: Voltea el cheque y firma tu nombre en el reverso en el área designada para el endoso. Asegúrate de que tu firma coincida con la registrada en el banco.

- Visita tu Banco: Dirígete a la sucursal local del banco donde tienes una cuenta. Lleva una forma válida de identificación, como una licencia de conducir o pasaporte.

- Acércate a un Cajero: Dependiendo de tu preferencia y de las opciones del banco, puedes presentar el cheque a un cajero para su procesamiento o usar un cajero automático equipado con la funcionalidad de depósito de cheques para obtener tu dinero.

- Proporciona Información Necesaria: Si estás tratando con un cajero, es posible que necesites proporcionar información adicional de la cuenta, como tu número de cuenta, banco emisor y el monto del cheque. Para depósitos en cajeros automáticos, sigue las indicaciones en pantalla para ingresar los detalles relevantes.

- Confirma el Depósito o Recibe el Dinero: Después del procesamiento, recibirás una confirmación del depósito en tu cuenta o el efectivo en mano si optaste por cobrar el cheque.

'Cobrar' un Cheque Electrónicamente

Además de los métodos tradicionales en persona, muchos bancos ofrecen opciones electrónicas para depositar cheques. Este enfoque conveniente te permite depositar cheques sin visitar ubicaciones físicas o incluso cobrar cheques sin identificación. Así es como funciona:

- Depósito Móvil: La mayoría de los bancos proporcionan una aplicación móvil que te permite depositar cheques usando tu smartphone o tableta. Simplemente endosa el cheque, toma fotos del frente y reverso, y envíalas a través de la aplicación.

- Banca en Línea: Algunos bancos ofrecen portales de banca en línea donde puedes escanear y cargar imágenes de cheques para su depósito. Este método generalmente sigue pasos similares al depósito móvil y es accesible a través de un navegador web.

- Transferencia Electrónica de Fondos: En algunos casos, puedes tener la opción de transferir electrónicamente los fondos de un cheque directamente a tu cuenta sin necesidad de procesamiento físico.

Pros y Contras de las Cuentas de Cheques

Las cuentas de cheques sirven como el centro para muchas transacciones financieras, ofreciendo tanto beneficios como desventajas. Comprender estos pros y contras es crucial para gestionar efectivamente tus recursos.

Ventajas de Tener una Cuenta de Cheques

- Conveniencia: Las cuentas de cheques proporcionan una forma conveniente de acceder y gestionar tus fondos para gastos diarios, como pagar facturas y hacer compras con una tarjeta de débito.

- Escritura de Cheques: Con una cuenta de cheques, puedes emitir cheques a personas o negocios, ofreciendo un método de pago seguro y rastreable.

- Depósito Directo: Muchos empleadores ofrecen depósito directo, permitiendo que tus cheques de pago se depositen automáticamente en tu cuenta de cheques, proporcionando acceso rápido al dinero.

- Banca en Línea: La mayoría de los bancos ofrecen servicios de banca en línea para cuentas de cheques, lo que te permite monitorear la actividad de tu cuenta, transferir dinero y pagar facturas desde la comodidad de tu hogar o en movimiento.

- Protección Contra Sobregiros: Algunas cuentas de cheques vienen con opciones de protección contra sobregiros, que pueden ayudar a prevenir transacciones rechazadas y tarifas en caso de fondos insuficientes.

Desventajas o Limitaciones de las Cuentas de Cheques

- Tarifas: Algunas cuentas de cheques y del mercado monetario pueden tener tarifas de mantenimiento mensual, tarifas por sobregiros, retiros limitados o tarifas en cajeros automáticos, que pueden reducir tu saldo si no se gestionan cuidadosamente.

- Requisitos de Saldo Mínimo: Ciertas cuentas de cheques requieren que mantengas un saldo mínimo para evitar tarifas, lo cual puede ser un desafío para quienes viven de cheque en cheque.

- Intereses Limitados: Aunque algunas cuentas de cheques ofrecen intereses sobre los saldos, las tasas son típicamente más bajas en comparación con las cuentas de ahorro, resultando en ganancias mínimas sobre tus depósitos.

- Riesgo de Fraude: Emitir cheques o usar una tarjeta de débito vinculada a tu cuenta de cheques te expone al riesgo de fraude o transacciones no autorizadas, lo que requiere vigilancia y reporte rápido de cualquier actividad sospechosa.

Al sopesar cuidadosamente las ventajas y desventajas de las cuentas de cheques y considerar factores clave al seleccionar la cuenta adecuada, puedes gestionar efectivamente tus finanzas y aprovechar al máximo tu experiencia bancaria.

Dónde Cobrar un Cheque

Cuando se trata de cobrar un cheque, tienes varias opciones disponibles, que van desde un banco tradicional hasta una tienda minorista. Sin embargo, no todos los lugares son iguales, y es esencial sopesar los pros y los contras de cada opción antes de tomar una decisión.

Opciones para Cobrar Cheques, Incluyendo Bancos y Tiendas Minoristas

- Bancos: Tu banco a menudo es la opción más sencilla para cobrar un cheque. Puedes visitar una sucursal o usar un cajero automático equipado con funcionalidad de depósito de cheques. Muchos bancos y cooperativas de crédito también ofrecen opciones de depósito móvil, lo que te permite depositar cheques usando tu smartphone.

- Tiendas Minoristas: Algunas tiendas minoristas, como supermercados, tiendas de conveniencia y minoristas grandes, ofrecen servicios de cobro de cheques por una tarifa. Esta puede ser una opción conveniente si no tienes una cuenta bancaria o necesitas acceso a efectivo fuera del horario bancario.

- Tiendas de Cobro de Cheques: Las tiendas dedicadas al cobro de cheques se especializan en cobrar cheques por una tarifa. Aunque estos establecimientos proporcionan acceso rápido al efectivo, sus tarifas pueden ser más altas en comparación con otras opciones, reduciendo la cantidad que recibes.

- Tarjeta de Débito Prepagada: Ciertas tarjetas de débito prepagadas te permiten cargar cheques en la tarjeta electrónicamente, proporcionando acceso instantáneo a los fondos. Esta puede ser una opción conveniente si usas regularmente tarjetas prepagadas para transacciones financieras.

Dónde Evitar Cobrar un Cheque Debido a Tarifas Potenciales o Limitaciones

- Prestamistas de Pago Diario: Evita cobrar cheques en establecimientos de préstamos de pago diario, ya que a menudo cobran tarifas exorbitantes y pueden involucrarse en prácticas de préstamos depredadores.

- Casas de Empeño: Aunque algunas casas de empeño ofrecen servicios de cobro de cheques, sus tarifas pueden ser altas y pueden requerir garantía o imponer tasas adicionales y más dinero para cubrir transacciones.

- Minoristas con Altas Tarifas: Ten cuidado al cobrar cheques en minoristas que cobran tarifas altas por el servicio, ya que estas tarifas pueden reducir significativamente la cantidad de efectivo que recibes.

Al decidir dónde cobrar un cheque, considera factores como la conveniencia, las tarifas y el acceso al dinero. Opta por un establecimiento y servicio reputados con estructuras de tarifas transparentes para asegurarte de obtener el mayor valor de tu experiencia de cobro de cheques.

Comparación de Cuentas de Cheques y de Ahorros

Entender las diferencias entre las cuentas de cheques y de ahorros es crucial para una gestión financiera efectiva. Aquí tienes una comparación concisa:

Tasas de Interés y Beneficios de las Cuentas de Ahorros

- Tasas de Interés: Una cuenta de ahorros generalmente ofrece tasas de interés más altas en comparación con una cuenta de cheques, lo que la hace ideal para hacer crecer tu dinero con el tiempo.

- Beneficios:

- Ahorro Orientado a Metas: Las cuentas de ahorros son excelentes para destinar fondos a metas específicas.