Immigration

How to Create a Resume in the United States: Step-by-Step + Template

Learn how to create a resume to find a job in the United States, how to pass ATS filters, common mistakes to avoid, and templates to adapt yours.

8 min read

18 Dec 2025

Practical Guide + Template to Create Your Resume in the United States

Getting a stable and well-paid job is the main goal of thousands of immigrants who come to the United States in search of a better quality of life.

For this reason, it’s essential to have an optimized resume (“CV”) that summarizes personal information, work experience, academic background, and all relevant details for recruiters and hiring managers.

You’ve probably faced the challenge of writing and refining a CV to apply for a job in your home country.

However, knowing the standards in Latin America is not enough, as U.S. resumes have key differences, such as length and focus on measurable results.

Mastering a new resume format can be challenging, and the process can be frustrating if you don’t hear back after sending multiple applications.

This doesn’t necessarily mean you lack the required skills — your resume might simply need some adjustments to get noticed by U.S. recruiters.

In this article, we aim to make the process easier for immigrant job seekers through a complete guide and sample resumes that will help you create your own by the end of the reading.

Differences Between a U.S. Resume and a Latin American CV

Even if you know how to write a resume in Latin America, it’s essential to understand the key differences compared to the U.S. standard.

Here are the main differences between a professional CV in Latin America and a U.S. resume.

- Length

In Latin America, it’s common to see two-page CVs, while the American resume is usually limited to one page.

- Focus on Quantifiable Achievements

U.S. recruiters look for quantifiable data and measurable results, while in Latin America it’s more common to include task descriptions and responsibilities.

- No Photo, Age, or Marital Status

To prevent discrimination, U.S. resumes do not typically include a photo, age, or nationality.

- Use of Keywords to Pass ATS Filters

The use of ATS (Applicant Tracking Systems) to detect keywords is widespread among U.S. companies.

- Format

While Latin American CVs often use colorful or elaborate designs, U.S. recruiters prefer minimalist formats to make information easier to read.

Understanding these differences is crucial for immigrants, as it increases the chances of being considered by both recruiters and automated systems.

7 Steps to Create a Resume in the United States

Here’s a step-by-step guide to writing a strong U.S. resume that passes ATS filters and captures recruiters’ attention.

Step 1. Choose the Right Format

Avoid flashy designs, as they can make reading difficult and hurt your ATS score. Choose a clean, organized, and easy-to-scan format.

Step 2. Fill in Your Contact Information

Include your full name, U.S. phone number, professional email address, and LinkedIn profile link.

Remember that you do not need to include a photo, date of birth, or marital status.

Step 3. Write Your Professional Summary

Your profile should be concise and include relevant keywords. This section should be a short paragraph summarizing your work history, interests, achievements, and career goals.

Step 4. Clearly Present Your Work Experience

It’s essential to list your work experience clearly and in chronological order.

- Use bullet points to list your most recent positions, including company name, job title, start and end dates.

- Highlight measurable achievements in each position.

To write your professional achievements, use the XYZ formula, structured as follows:

- X: what you did

- Y: how you did it

- Z: the result achieved.

For example:

“Improved the brand’s visual identity through an e-commerce rebranding project, reducing cart abandonment by 50%.”

Step 5. Your Education

List your academic background, including institution name, degree, and attendance dates.

Step 6. Highlight Your Skills

The skills section is key to making your resume stand out.

It’s recommended to separate this section into soft skills and technical skills.

- Soft skills: communication, teamwork, time management, attention to detail.

- Technical skills: design and editing software.

Step 7. Optional Sections

Depending on the vacancy and your profile, you can include additional sections, such as languages, certifications, or volunteer experience.

This information can set you apart from other candidates, as it gives you additional skills that could be relevant to the position.

Example of a U.S. Resume

Here’s an example of how an optimized resume should look, according to U.S. company standards.

On this page, you can download CV templates in English to customize yours according to your experience.

The last step is to adapt this example to your own professional profile and career path, which may differ depending on whether you are a recent graduate or already have experience.

- Recent graduate: if you have no experience, focus on your academic background, highlighting valuable projects, professional internships, volunteer work, and personal projects.

- Professional with experience: adapt the example to your own work history and use the XYZ formula to highlight your professional achievements.

Common Mistakes to Avoid When Writing a Resume in the U.S.

Here are some things to avoid when writing your resume.

- Using the same resume for every job: try to tailor your resume to the job you are applying for.

- Including a photo or unnecessary personal details: remember that in the United States, this data is irrelevant.

- Poorly translating key terms: if you have doubts about how to translate a term from Spanish to English, consult a translator or compare different sources on the internet.

- Making it too long: your resume should not exceed one page; otherwise, it may be discarded even if you have the necessary skills.

- Using a graphic-heavy design that doesn’t pass ATS filters: you may think that recruiters like resume templates with eye-catching designs, but the truth is that they are unlikely to pass ATS filters.

Común, Your Ally for Financial Stability in the United States

Having a strong resume is key to successfully entering the U.S. job market.

Just as a resume opens the door to great job opportunities, Común opens the door to financial stability for immigrants.

Discover Común, the option designed to serve the needs of immigrant communities in the U.S., with service available in Spanish.

Discover All the Benefits of Común!

- Open a checking account with a qualifying official identification from your home country.

- Mobile app available in Spanish and English.

- Easily receive payments from employers, cash checks, and send international money transfers to Latin America.

Discover Común, the option dedicated to meeting the needs of immigrant communities in the United States with services available in Spanish.

Frequently Asked Questions (FAQ)

If you still have questions, check out the next section.

Is It Necessary to Include References in the Resume?

It’s not necessary to include references in your resume, as companies usually request them later in the hiring process.

What Are the 3 Most Important Details in a Resume?

The 3 most important details are: contact information, professional experience, and skills.

What Language Should My Resume Be In When Applying in the U.S.?

The resume format used in the U.S. is becoming common in other countries, so the language should match the job posting.

About Común

Común aims to support the Latino community in the United States. It offers a debit account that can be opened with more than 100 valid Latin American IDs and an app available in Spanish.

Visit Común's website or download the app for free to learn more about the full offer and applicable terms.

Olivia Rhye

Community Partner

Living in the United States

How to Get a Driver’s License in the United States as a Foreign National

8 min de lectura

Driver’s license in the United States for foreign nationals: steps and requirements

Having a driver’s license makes everyday tasks easier, such as going to work, the supermarket, school, medical appointments, and more. This process is especially important for immigrants living in the United States, as it gives them independence and stability in the country.

Although the process to obtain a driver’s license varies in each state, foreign nationals do have the possibility and the right to obtain one. Below, we explain all the details so you can get this permit soon.

Can you drive with an international license in the United States?

If you have recently arrived in the United States and need to get around in your own car, you may temporarily use the driver’s license from your home country, as long as it is issued in English or accompanied by an international driving permit.

As a new driver in the United States, you must understand the difference between an international license and a local one: the former supplements your national license and allows you to drive in the U.S. for a few months; the latter is issued by the Department of Motor Vehicles (DMV) in each state and grants you a permanent permit to operate a motor vehicle in the country.

Regulations differ in each state: for example, in California you can drive with a valid foreign license until you become a resident. In contrast, in Texas your national license is valid for 90 days, and you must always carry your passport or visa.

Allowed period to drive with a foreign license

The maximum time allowed to drive with a foreign license varies depending on each state’s local regulations. In general, the period can range from 30 days to one year, from the day you arrive until you establish yourself as a permanent resident.

When is it necessary to apply for a U.S. driver’s license?

If you plan to live in the United States for a longer period, you need a U.S. driver’s license to drive. It is also essential if you plan to buy a car.

Also, remember that in some states the period to drive with a foreign license is limited, so you should consider applying for a U.S. license before that deadline expires.

Requirements to obtain a driver’s license in the U.S. as a foreign national

The requirements to obtain a driver’s license also vary by state, although the general structure is similar.

This is the documentation needed to obtain a driving permit in the United States.

- Valid passport or official identification: used as proof of identity.

- Proof of residency: can be a utility bill, rental agreement, or official letter showing your address.

- Immigration status or proof of legal presence: such as the Employment Authorization Document (EAD) or the I-20 form for students.

- Social Security Number (SSN) or an SSA ineligibility letter.

Keep in mind that states such as New York and Illinois allow applicants to obtain a driver’s license without considering immigration status.

Learn here how to send money without a bank account.

5 steps to apply for your U.S. driver’s license

Getting your driver’s license may seem like a complex and tedious process. In reality, you only need to stay organized and take the time to understand the guidelines.

Step 1. Gather your documents

Before going to a DMV office, make sure to prepare the required documents. In the previous section we outlined what you generally need, but remember to check for variations in the state where you live.

Step 2. Schedule an appointment at the DMV

Then, visit the DMV website and book an appointment. On the scheduled day, your documents will be reviewed and you will be given a date for the written exam.

Step 3. Take the written exam

The written exam evaluates your knowledge of traffic rules and road safety. Each state offers a driver’s manual to study for the test, and some are available in other languages, such as Spanish.

If you pass, you will receive a learner’s permit that will allow you to take the driving test under the guidance of an instructor.

Step 4. Take the driving test

The next step is probably the most challenging, as you must apply your theoretical knowledge in real driving practice. During the test, the instructor will evaluate your ability to follow traffic signs, park, turn, and follow safety rules.

Step 5. Pay the corresponding fees

Once you pass your driving test, you must pay a fee that varies by state. Initially, you will receive a temporary license and later receive your permanent license by mail.

Costs, timelines, and validity of a U.S. driver’s license

The cost of a driver’s license in the United States depends on each state, but generally includes the cost of the written exam, driving test, and issuance. The validity also varies by state, but it is usually between 4 and 8 years.

Additionally, a positive update for immigrants is that more states are removing immigration status requirements to issue a driver’s license; this is the case in California, New York, and Illinois.

If you have questions about the specific requirements in your state, check the updates on the official DMV website.

Drive toward your financial independence with Comun

Having a U.S. driver’s license represents another step toward achieving financial independence and making it easier to move around your city. Therefore, it is essential to understand the process to obtain one, as well as the differences in each state.

In other words, having a license simplifies and improves your life by making everyday tasks more accessible. Likewise, Comun is the financial platform that helps you manage your money safely and without complications.

Open your account with Comun and take the next step toward your independence in the United States. Manage your money with confidence, clarity, and support at every step.

Frequently Asked Questions (FAQ)

If you still have questions, check the following section.

How long can I drive with my foreign license in the U.S.?

The duration varies depending on the state you are in, but generally ranges from three months to one year.

What happens if my immigration status changes after I obtain my license?

If your immigration status changes after you obtain your driver’s license, it is recommended to update your information at the DMV. You may need to apply for a new license or present updated immigration documentation.

Is it valid to use an international license in all states?

Although the international driving permit (IDP) is accepted in most states, it must be accompanied by a valid national license. Additionally, there may be restrictions on how long it can be used in each state.

Can I get a driver’s license without a Social Security Number (SSN)?

Yes, it is possible to apply for a driver’s license without an SSN in several states. In this case, you must present an ineligibility letter issued by the Social Security Administration (SSA).

Financial Education

How to Invest Money in the United States: A Beginner’s Guide

8 min de lectura

Ways to Invest Money and Secure Your Future in the United States

One of the constant concerns for people who leave their home country in search of better opportunities in the United States is financial uncertainty, often caused by poor management and a lack of knowledge about effective strategies to grow their money.

Saving products are an alternative that allows you to save money in the long term while earning interest—returns that depend on the term and the rate offered by the financial institution.

Knowing the different ways to save money is a way to ensure financial stability for you and your family. Below, we explain the types of investments and the safest ways to get started. Please note that investment products are NOT FDIC INSURED, NOT BANK GUARANTEED, and MAY LOSE VALUE.

What Does It Mean to Invest Money and Why Is It Important?

Investing means allocating money toward a goal with the aim of obtaining higher returns in the future. You can do it on your own, through a business, or with formal financial instruments that put the contributed money to work to pay interest over defined time frames.

Here are some benefits of using investment strategies:

- Financial security: gives you the confidence of having a savings fund for the future.

- Financial growth: puts your money to work to generate passive income and avoid losing value due to inflation.

- Family support: helps you plan long-term family projects, such as buying a home or paying for children’s higher education.

How to Define Your Goals and Risk Profile Before Investing

Before you begin, keep in mind that all investments involve some level of risk. If you’re a beginner, it’s essential to start at a level that matches your situation.

You should also be clear about your financial goals—the targets you want to reach in the short, medium, and long term.

Risk Profile

A risk profile is an investor’s ability to handle potential losses caused by market fluctuations.

These are the three main types.

Conservative

This profile is ideal for people not familiar with investing, as it involves low risk. Although returns are steady, they tend to be lower than other investment alternatives. Preferred options include savings accounts and short-term investment funds.

Moderate

This profile suits somewhat more experienced investors who are willing to take moderate risk by combining safer investments with slightly riskier ones to obtain better returns.

Aggressive

This profile is for those who have a strong command of investing. They have a high tolerance for losses and aim for high income through significant long-term investments, typically in the stock market, high-yield funds, and real estate.

Determine Your Risk Profile

Next, define the risk profile that aligns with your personal finances and your experience with these instruments.

Follow these tips to help you make a smart investment.

Step 1. Assess Your Current Financial Situation

Take stock of your finances—consider your income, monthly expenses, debts, and existing savings.

Step 2. Determine Your Investment Goals.

Set exactly what you want to achieve and in what timeframe—for example, buying a home, traveling abroad, paying for medical treatment, or simply building an emergency fund. Remember that long-term investments involve higher risk but can also offer higher returns.

Step 3. Decide How Much You Can Invest Initially.

Based on your budget, determine how much you can allocate to your initial investment and whether you can increase it later.

Step 4. Evaluate Your Risk Tolerance.

Analyze your willingness to accept potential losses and their impact on your personal finances.

Here is a comparative table for clarity.

Investment Profile

Risk Level

Time Horizon

Potential Return

Characteristics

Conservative

Low

Long – Medium

Low

Prioritizes safety over return.

Moderate

Medium

Medium – Long

Low – Medium

Balances safety and returns.

Aggressive

High

Long

High

Seeks to maximize long-term gains, with higher risk.

4 Accessible Investment Options for Beginners

A common misconception is that you need a significant amount of money to become an investor. In reality, there are accessible alternatives that let you start with small amounts, easily.

Here are four ideal options to start investing.

Index Funds

Index funds pool money from multiple investors to buy stocks or bonds.

Main Benefits:

- Automated operation.

- Easy diversification.

- Potential for good long-term returns with little effort.

Certificates of Deposit (CDs)

A certificate of deposit is an investment made directly with a financial institution for a fixed term, meaning you cannot withdraw the money during that period.

Main Benefits:

- A relatively secure way to start investing, as it’s offered by financial institutions.

- Generates steady, predictable returns.

Bonds

Bonds are loans to companies or governments that pay interest periodically and generally carry lower risk.

Main Benefits:

- Income is more predictable.

- A good option to diversify alongside slightly riskier investments.

Digital Investment Accounts

An accessible option that allows you to invest from a mobile application.

Main Benefits:

- Let you start with very small amounts of money.

- Very beginner-friendly for entering the world of investing.

Before choosing an investment vehicle, consider your risk profile. If you prefer stability over returns, CDs or bonds may be ideal.

Avoid “putting all your eggs in one basket.” The key to smart investing is diversifying across several instruments, even with small amounts.

Simple Habits to Invest and Review Your Strategy

When you start investing, it’s important to be realistic, stay patient, and remain consistent with your financial goals.

Here are some simple practices to keep your investments on track.

- Review your investments at least every 3 to 6 months.

- Adjust your strategy as your goals or financial situation change.

- Use digital tools to monitor your progress.

Use Común to Manage Your Money Easily as an Immigrant in the U.S.

Financial management is a responsibility you should entrust to an accessible platform.

Meet Común! The financial service that lets you send, receive, and withdraw money within and outside the United States, quickly, simply, and securely.

Común is a mobile app that allows you to open an account easily with a qualifying official identification from your home country, so it’s a great option for the immigrant community.

Open your account with Común and start sending, receiving, and withdrawing money. Enjoy Spanish and English language support, clear fees, and a digital platform ideal for the immigrant community in the United States.

Frequently Asked Questions (FAQ)

If you still have questions, see the section below. Please note that investment products are NOT FDIC INSURED, NOT BANK GUARANTEED, and MAY LOSE VALUE.

How much money do I need to start investing in the U.S.?

There are quite accessible investment options today, especially digital platforms. Some let you start with amounts as low as $1 or $5, which is ideal for learning to invest.

Is it safe to invest as an immigrant?

Yes—even if you are not a legal resident, you can invest money in the United States. Just make sure to use regulated institutions and platforms.

What if I want to change my investment strategy in the future?

It’s common to change your investment strategy to match your financial goals. Review your investments periodically and make the necessary adjustments according to the applicable timelines.

Living in the United States

Websites for finding jobs in the USA: 2026 guide for immigrant workers

8 min de lectura

Websites for finding jobs in the USA (2026 guide for immigrant workers)

An essential guide for finding a job in the USA. The search for a job in a new country can be a challenge, many processes may feel new or unfamiliar. However, in 2026 there are plenty of online resources to help with the process, one of the most commonly used resources is online job platforms. For many Spanish-speaking employment seekers in the USA whether recently arrived or supporting a family, there are employment opportunities available, the key is to know where to find them.

To help with the search, we have created a guide designed as a practical, curated overview of the most relevant websites for finding jobs in the United States. We hope to provide useful context on which platform works best depending on your situation.

The 10 best websites for finding jobs in the USA

1. Indeed

A practical starting point

Among all job platforms in the United States, Indeed continues to be the most widely used, especially for people looking for entry level or widely available opportunities. Its main advantage is volume. It gathers thousands of listings across industries from restaurants, warehouses, cleaning services, retail, to customer service. The platform allows users to apply for many positions directly through the app or website.

However, this same ease of use means competition is high. Users of the platform have reported that, for better chances of success, it is important to apply early and consistently.

Available in Spanish?

Indeed is fully available in Spanish, it is one of the most complete Spanish experiences among all websites for finding jobs in the USA.

2. LinkedIn

For professional and office roles

LinkedIn is more about building a professional presence. Therefore it is very important to have a well structured profile with recommendations and references to all previous experiences to attract potential opportunities.

This platform is commonly used for roles in administration, marketing, finance, and technology. The platform is generally more focused on professional and corporate roles than hourly positions. It is also important to consider that finding a job through it tends to take some time.

Available in Spanish?

LinkedIn is partially available in Spanish. It allows you to change the interface to Spanish, including menus and profile sections. However, most job postings in the USA and recruiter interactions are still primarily in English.

3. Glassdoor

For researching companies

Glassdoor is not just a job board; it is a decision-making tool. While it does include job listings, its real value lies in the information it provides about companies. Users can see salary ranges, employee reviews, and even details about the interview process.

For someone unfamiliar with the U.S. labor market, this can be helpful when evaluating workplace conditions and company culture and help identify companies with better working conditions. Many job seekers use Glassdoor alongside other job search websites in English and Spanish to confirm whether a job is worth pursuing before applying.

Available in Spanish?

Glassdoor is partially available in Spanish. It offers some Spanish interface options and content, but the experience is mixed. The reviews and salary data are often in English, depending on the company. It is still useful, but not fully localized.

4. ZipRecruiter

Faster matching with less effort

ZipRecruiter focuses on simplifying the job search by using technology to match candidates with relevant opportunities. Instead of spending hours browsing, users receive recommendations based on their profile, and in some cases, some employers may contact candidates directly.

This approach is particularly helpful for candidates with some work experience who want to save time and avoid repetitive applications. It reflects how job platforms in the United States are evolving toward more automated and personalized systems.

Available in Spanish?

ZipRecruiter is mostly in English. It is primarily an English-language platform.

5. SimplyHired

Useful for understanding salaries

SimplyHired plays a valuable supporting role. It aggregates listings from multiple sources and provides salary estimates that help job seekers understand what a position typically pays.

For newcomers trying to navigate where to find work in the USA, this information is especially useful. It helps with comparing offers and may help job seekers better understand local ranges.

Available in Spanish?

SimplyHired is partially available in Spanish. It has some Spanish interface support and localized search options. However, like other platforms, many listings remain in English.

6. USAJobs

The official path to government work

USAJobs is the official federal employment portal. It offers access to government positions, which are known for stability, structured hiring processes, and strong benefits.

However, it is important to be realistic about accessibility. Most roles require legal residency or U.S. citizenship, which may limit eligibility for some applicants.

Available in Spanish?

USAJobs offers limited Spanish support. It is mainly in English, as it is the official government portal.

7. FlexJobs

A path to find remote work

As remote work continues to grow, FlexJobs has become one of the most reliable platforms in this space. Unlike larger job boards, it focuses on curated listings, which may help reduce exposure to fraudulent or low-quality listings.

This makes it particularly useful for people looking for flexibility, whether they are freelancers, parents, or simply prefer not to work in a traditional office setting. In the context of websites for finding jobs in the USA, it stands out for prioritizing quality over quantity.

Available in Spanish?

FlexJobs operates almost entirely in English.

8. Upwork

A practical option for remote income

Upwork allows users to work as independent contractors, offering services in areas such as writing, programming, design, and digital marketing. It has become one of the most relevant platforms for remote work, especially as companies increasingly hire global talent.

While it requires time to build a profile and reputation, some users use it to generate freelance or supplemental income and open doors to long-term clients. It is particularly useful for people with digital skills who are looking for flexibility.

Available in Spanish?

Upwork offers a Spanish interface, which makes it more accessible than many remote platforms. However, most clients post jobs in English.

9. Fiverr

For turning skills into income

Fiverr offers a slightly different model from Upwork. Instead of applying to jobs, users create service listings and set their own prices, allowing clients to find them directly.

It is commonly used for creative work and as a source of side income, but it can also grow into a full-time opportunity. Within the broader landscape of job search websites in English and Spanish, Fiverr stands out for its flexibility and accessibility.

Available in Spanish?

Fiverr also supports Spanish in its interface. Since you create your own service listings, you can write them in Spanish, English, or both, which gives you flexibility depending on your target clients.

10. The Muse

A more curated, culture-focused option

The Muse is smaller than other platforms but offers a more curated experience. It focuses on companies that prioritize workplace culture and transparency, giving candidates a clearer idea of what to expect.

This makes it particularly appealing for younger professionals or those looking for a better long-term fit rather than just immediate employment. While it may not be the first stop for most job seekers, it can be a valuable complement to larger platforms.

Available in Spanish?

The Muse is primarily an English-language platform with no full Spanish interface.

Choosing the right platform for your situation

These platforms are useful within their unique context, the key to making the most out of them is understanding what they offer and how they fit in your situation. Someone looking for quick, entry-level work will likely benefit most from Indeed, while a candidate pursuing a long-term professional career should prioritize LinkedIn. Those interested in flexibility or remote income may find better results through FlexJobs, Upwork, or Fiverr, while individuals seeking long-term stability may consider USAJobs if they meet the requirements.

In practice, the most effective strategy is not to rely on a single platform. Combining two or three of these tools creates a more balanced approach and may improve job search efficiency.

How to apply without an SSN or with an ITIN

When exploring websites for finding jobs in the USA, one practical question often comes up early in the process: what happens if you don't yet have a Social Security Number (SSN)? In most formal employment situations, an SSN is required because employers use it for payroll and tax reporting. However, during the application stage, many platforms still allow you to apply without entering one.

If you already have legal work authorization but are waiting for your SSN, you can:

- Typically move forward in the hiring process, if the employer allows, and provide the number later

- In some cases, employers may accept an Individual Taxpayer Identification Number (ITIN) for tax purposes (although it does not replace work authorization)

The key distinction is that an ITIN allows you to comply with tax obligations, but it does not grant permission to work.

Requirements can vary depending on the employer and the type of role, therefore it is important to confirm what documentation will be needed once you move forward in the hiring process.

Tips for preparing your application

Using the right job platforms in the United States is the first part of the process. How you present yourself still plays a major role in whether you get a response.

- A strong resume should be clear, concise, and tailored to the type of job you are applying for

- In the U.S., resumes are typically one page and focus on skills and results rather than long descriptions

- Adjusting your resume to include keywords from the job description may help resumes align with automated application systems used by some employers

When it comes to interviews, preparation is just as important:

- Employers often expect candidates to explain their experience clearly and give examples of past work

- If you are not fluent in English, practicing common questions in advance can help you feel more confident

Applying regularly, following up when appropriate, and staying organized throughout the process may help improve consistency throughout the job search.

After you get the job: getting paid

Once you are successful and you find work in the United States, it is important to know how and where you are getting paid. Most employers rely on direct deposits, which requires access to a U.S. bank account. For many immigrants, this can be a challenge. Some financial institutions and fintech platforms offer products designed for individuals who may have limited access to traditional banking services. From traditional banks to digital platforms it's important to learn about their requirements and their offers. For example, with Común you can open a debit account using a passport or more than 100 valid Latin American IDs and Común's app is available in Spanish.

Frequently Asked Questions

Do I need a work permit to work in the United States?

Yes. To work legally in the U.S., you must have valid work authorization. This typically comes in the form of a work permit (Employment Authorization Document, or EAD) or a visa that allows employment.

What types of work permits are available for immigrants?

There are several common pathways depending on your situation. Temporary work visas like the H-2A (agricultural work) and H-2B (seasonal non-agricultural work) are frequently used. Professional visas such as the H-1B apply to specialized roles, while other options like TPS (Temporary Protected Status) or asylum-based work permits may apply depending on your country of origin and circumstances.

Each option has specific requirements, so it is important to verify eligibility with the official authorities.

Can I work in the United States if I don't speak English?

Yes, it is possible. Many jobs, especially in construction, cleaning, manufacturing, agriculture, and restaurants do not require advanced English. In cities with large Latino populations, it is common to find Spanish-speaking work environments.

However, improving your English can significantly expand your opportunities and increase your earning potential over time.

What are employment agencies?

Employment agencies, also known as staffing agencies, act as intermediaries between companies and job seekers. They help match candidates with available positions, often for temporary, seasonal, or entry-level roles.

For many newly arrived immigrants, these agencies may help some job seekers connect with available opportunities, especially if someone does not yet have a strong professional network in the United States.

Final thoughts

The key to navigating the U.S. job market in 2026 is not just knowing the websites for finding jobs in the USA, but understanding how to use them strategically. Each platform serves a different purpose, and choosing the right one may help better organize search and identify opportunities aligned with goals and experience. We wish you the best of luck in your job seeking process!

Financial Education

What is ACH and why is it important for sending and receiving money in the U.S.?

8 min de lectura

If you need to make bank transfers in the United States, it will be useful to know what the ACH network is and understand its importance in the country’s banking system.

ACH (Automated Clearing House) is an Automated Clearing House that handles the processing of electronic transfers between U.S. accounts.

It is highly relevant for receiving direct payroll deposits, also known as ACH credits, and for processing recurring payments, due to several advantages compared to the traditional bank network, such as cost reduction and traceability of operations.

According to official sources, in 2024 the ACH payment network processed around 33.6 billion electronic payments, with a value close to $86.2 trillion, underscoring the importance of this method in the U.S. financial system.

On this occasion, we will explain in detail the advantages of this type of transaction and provide some recommendations so you can get the most out of them.

What is ACH and how does it work?

ACH or Automated Clearing House is a network that allows money to move between banks, credit unions, and other financial institutions in the United States, where the use of cash or checks is not necessary, because everything is processed electronically.

The central part of this system is NACHA (National Automated Clearing House Association), which oversees compliance with the rules and ensures transfers are carried out according to established security standards.

It is very likely that in your daily life you have already used the ACH system without noticing it. For example, for:

- Payroll deposits: every time you receive your salary in your bank account.

- Bill payments: to pay basic services such as electricity and internet automatically.

- Transfers between people: when you make an electronic transfer to a friend or to your own accounts.

Differences between ACH payments and other transfer methods

In the United States, there are different systems for moving money. In addition to the ACH network, you can rely on more traditional networks such as wire transfers and checks.

The main difference with other bank transfer systems is that ACH focuses on electronic, secure, and low-cost payments, which take longer than other options that tend to be more expensive; whereas ACH transfers are more suitable for recurring payments and direct deposits.

Below, we show you a comparative table so you can visualize the fundamental differences between ACH payments and other methods.

| ACH | Wire transfer | Check | |

|---|---|---|---|

| Transaction speed | From 1 to 2 business days | From minutes to hours | From 2 to 5 business days |

| Cost per transaction | Free or reduced | Variable, around $25 to $50 USD | There may be issuance costs |

| Geographic availability | Only within the United States | National and international | National and sometimes international |

| Most common use | Payroll payments, bills, transfers between accounts, automatic payments | Transfers of large amounts of urgent money | Traditional payments between people without access to a bank account |

Benefits and some recommendations when using ACH payments

One of the main advantages of ACH payments is the security involved in using this system to transfer money. This is because it is regulated by an organization called NACHA, which verifies each transaction based on financial system regulations, thereby reducing the chances of fraud.

Despite the trust that ACH transfers provide, they also present some limitations.

These are the most common benefits and limitations of the ACH system:

Benefits

- It is the lowest-cost method of transferring money, as transactions are free or have minimal fees

- Transactions are protected by NACHA regulations, which guarantees their security

- It is a system well-suited for processing recurring payments and subscriptions

- It is easy to track operations, because all are recorded in the banking system

Limitations

- Transactions take longer to complete. Generally, they are reflected the next day or up to two business days later

- International money transfers cannot be made, only within the United States

- Some banks may set daily limits, so it is not advisable for moving large amounts of money

If you need an alternative for making recurring payments and direct deposits to a bank account within the United States, the ACH network is a popular alternative due to its security standards and accessibility. But if you are looking for other types of financial services, you can consider more comprehensive options.

At Común we make your ACH payments easier

As you can see, ACH payments are a reliable option for making and receiving money transfers, as long as they are scheduled transactions within the United States and within the limits set by banks.

It is very important to have a reliable and transparent partner to move your money and manage your personal finances in a comprehensive and efficient way.

Meet Común, the platform that integrates the ACH network for direct deposits, payments, and transfers, and uses a service that has clear and visible rates in the mobile app.

Discover everything Común offers you!

- Open your account with a qualified official ID from your country of origin—we accept more than one hundred of them!

- Get a debit card and make purchases easily

- Deposit cash at hundreds of locations near you

- Make international money transfers for a fee starting at $2.99 USD, up to the available limits

- Be part of a service that speaks your language and understands the needs of immigrants working in the United States

Don’t wait any longer—open your account at Común!

Frequently Asked Questions (FAQ)

If you have questions about what ACH is and what it is for, consult our Frequently Asked Questions section.

How long does an ACH transfer take?

Generally, ACH transfers take 1 to 2 business days. It is also possible they are completed the same day if the bank offers the same-day ACH option.

How much does it cost to send money via ACH?

ACH transfers are usually free up to the applicable limits. Some banks charge a minimal fee, around $3 USD. It is a more economical option than a wire transfer, which can cost more than $50 USD.

Is it safe to use ACH for personal payments?

Yes, ACH transfers are regulated by the NACHA system, so they are easily traceable and protected with anti-fraud security measures.

Can I use ACH if I don’t have a bank account in the U.S.?

No, to send money through the ACH system you need an account number from a U.S. bank or credit union. Otherwise, you can resort to more accessible alternatives such as Venmo, PayPal, and Común.

What is an ACH payment?

An ACH payment is a money transfer processed through the ACH system and managed by NACHA (National Automated Clearinghouse Association).

What is a wire transfer?

A wire transfer is a payment method that allows money to be moved from one bank to another electronically, both nationally and internationally.

Instant payments

Discover how to sign up for Zelle and move your money without complications

8 min de lectura

Are you looking for an option to send and receive money within the United States? In the digital era, it is essential to have access to an immediate, secure, and free transfer service.

Sometimes sending and receiving money can be challenging due to high fees or limited access to the banking system. For this reason, knowing how to register for Zelle and learning about alternative solutions such as Comun will be extremely useful for sending money without complications through the most efficient services.

In this guide, we will explain what Zelle is, how to register, what requirements are necessary to send and receive money, and why Comun works as a complementary solution to expand your options when facing restrictions that could hinder your access to mobile payment services.

What Is Zelle and How Does It Work for Your Daily Payments?

Zelle is a digital P2P (peer-to-peer) payment service available in the United States. It is associated with more than 20,200 traditional and digital banks and credit unions, such as Bank of America, Wells Fargo, Ally Bank, Capital One, and Navy Federal Credit Union. Zelle is well known for its wide coverage and ease of transferring funds between users of this system.

Other advantages of Zelle include:

- Near-Instant Transfers

Users can receive their money within minutes. - Ease of Use

It is directly linked to bank applications, eliminating the need for an external app. - Security

It is backed directly by banking institutions, so you can be confident that your money will reach its destination. - Usage Fees

You can send and receive money without paying commissions to other Zelle users.

Please note that Zelle is only available within the United States. If you need to make international transfers, find the best options here.

How Does Zelle Work?

Zelle operates through its connection with their affiliated banks’ applications. To send and receive money, you must first verify that your bank is part of this service’s network.

If so, complete your registration directly through your bank’s online platform and begin sending and receiving money to your account using a phone number or email address.

Using Zelle is very practical for daily transactions such as paying rent or purchasing goods and services. It is also a secure way to send money to family and friends.

In addition to Zelle, there are other alternatives for sending and receiving money within the United States. Discover the 6 best mobile apps of 2025.

What Changed in Zelle in January 2025?

Zelle announced an important change in its application that took effect in April 2025. The change consists of eliminating transfers through its standalone app, as the service can now only be accessed through the online banking platforms of U.S. financial institutions integrated into its network.

If you wish to download the Zelle app, you may still use it to review your payment history.

How to Download Zelle to My Phone: Key Requirements to Register and Use It Without Complications

To have a Zelle account, you only need to meet the following requirements:

- U.S. Mobile Phone Number or Email Address

To use Zelle, you only need to register a phone number and an email address. Your contacts can use either of these to send you money easily. - U.S. Bank Account

Since Zelle operates directly through bank connections, having an account with one of the institutions integrated into its network is mandatory.

Check the list of banks that offer Zelle on their website and ensure you will be able to use the service in 2025. - Banking Application

Finally, you must download your financial institution’s mobile banking app, as you will access Zelle through it.

What Can I Do If I Cannot Open an Account in the United States ?

Sometimes, opening an account is not accessible for many individuals, whether due to lack of required documentation or insufficient credit history.

If this is your situation, Comun is a great alternative for sending money to your loved ones safely, quickly, and at low cost.

Comun is a platform that understands the needs of immigrant communities in the United States. Open your account today and experience an accessible alternative for your finances.

4 Simple Steps to Register for Zelle

If you are wondering how to open a Zelle account, simply follow these steps:

1. Open Your Bank’s Mobile Application (If It Is a Zelle Partner)

Once you verify that your bank works with Zelle, open the mobile application and register if you have not done so yet.

2. Locate the Transfers and Payments Section

In the main menu, click on the transfers and payments section, then select “Send Money with Zelle.”

3. Register Your U.S. Phone Number or Email Address

To send and receive money with Zelle, it is necessary to register a U.S. phone number and an email address.

4. Link Your Bank Account

Confirm your information and start sending and receiving money with Zelle quickly after completing a test transaction.

With Your Comun Account, Make and Receive Payments Easily and Quickly

Undoubtedly, Zelle is an excellent tool for bank transfers, offering a fast and very simple service to use. Although it is only available to users of participating banks, it has broad coverage.

While Zelle represents a practical solution for many users, it has limitations such as requiring an eligible U.S. bank account.

Comun, on the other hand, is an alternative solution that goes beyond traditional limitations, as it allows you to send international transfers using your official national identification. It is designed for immigrants in the United States and offers simplified financial management. This service provides you with:

- A debit card to make purchases at physical establishments

- Access to a mobile app for better financial control

- The ability to send remittances to your loved ones for a fee starting at $2.99 per transaction up to the applicable limits

- The opportunity to join our community that understands your needs

Download the Comun app and enjoy transparent, easy, and personalized finance designed for you.

International Money Transfers

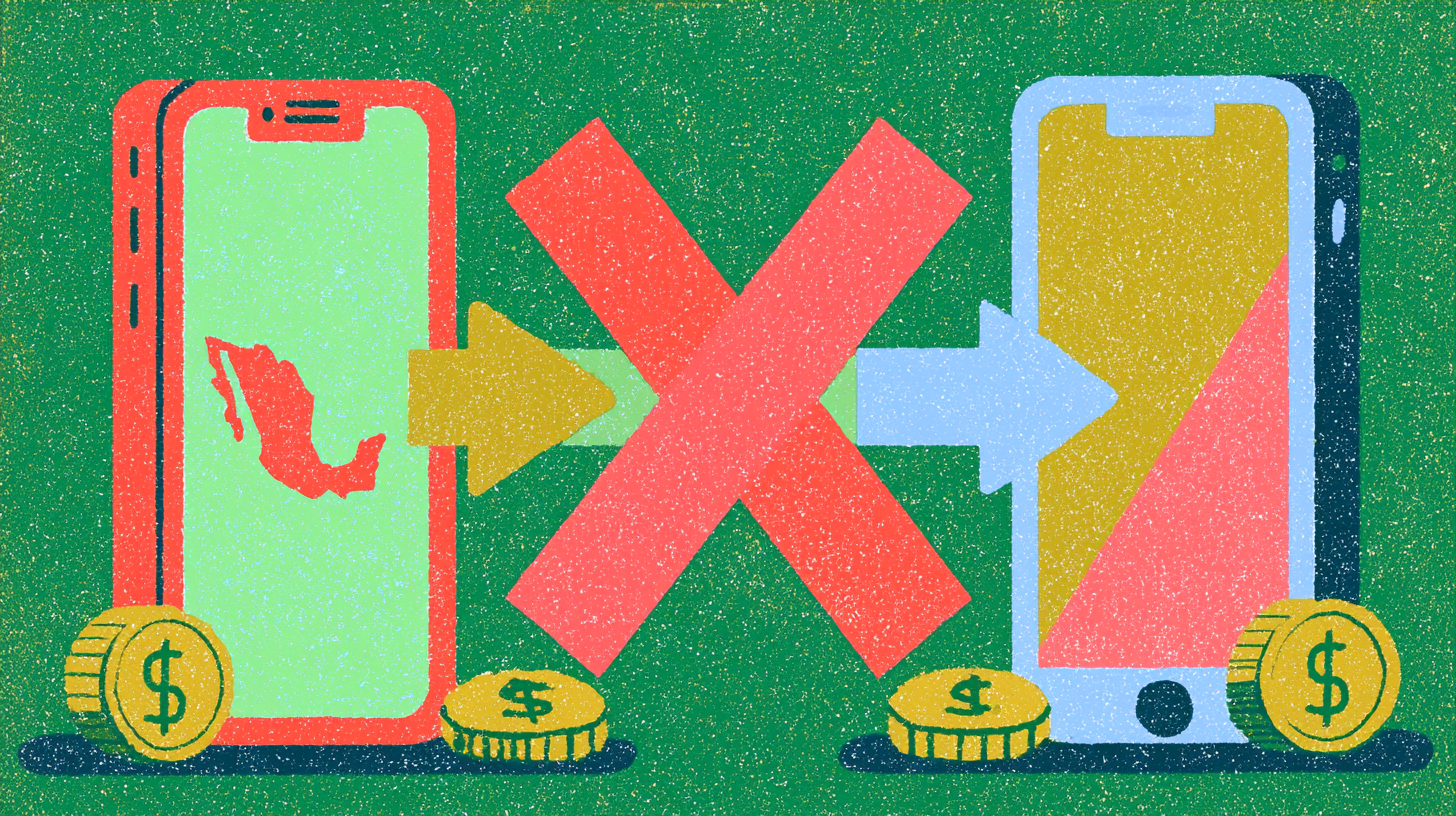

Which banks offer Zelle in Mexico? What you need to know in 2026

8 min de lectura

Which banks offer Zelle in Mexico? What you need to know in 2026

Zelle does not send money directly to Mexico. Zelle only works between eligible U.S. bank accounts and credit unions within the United States.

If you are looking into different methods for sending money to your family in Mexico, you may be searching for 'which banks offer Zelle in Mexico' or trying to understand if Zelle works internationally. This is a common misunderstanding for immigrant families in the U.S. No Mexican bank officially offers Zelle for receiving transfers from the U.S., and Zelle itself is not designed for international money transfers or currency conversion.

What is Zelle and how does it work?

Zelle is a digital payment service that facilitates peer-to-peer transfers at select partner banks in the United States. It is known for its speed, with transfers appearing in minutes, and for its extensive coverage across the U.S. Some U.S. financial institutions that support Zelle include Bank of America, Chase, Wells Fargo, Citi, PNC, and many more.

Why doesn't Zelle work for sending money to Mexico?

Cross-border money transfers require financial institutions, payment networks, regulatory approvals, identity verification procedures, and international settlement systems. Zelle was built around domestic payment systems in the U.S. Because of this, the service does not support direct transfers from U.S. bank accounts to recipients in Mexico.

Alternatives for sending money to Mexico from the U.S. (2026 comparison)

| Service | Typical starting fees | Delivery speed | Exchange rate model | Cash pickup |

|---|---|---|---|---|

| Remitly | Varies; ~$1.99+ for bank deposit to Mexico | Express: minutes to same day; Economy: 3–5 days | Exchange rate markup applies | Yes |

| Wise | From ~0.48% of transfer; shown upfront | Usually same day to 2 days | Mid-market rate, no markup | Limited (select corridors) |

| Xoom | Depends on payment method and destination | Minutes to 1 day | Exchange rate markup applies | Yes |

| Western Union | Varies widely by method and destination | Minutes to several days | Exchange rate markup applies | Yes (extensive agent network) |

| Común | Starts at $2.99 via UniTeller; may vary | Varies by destination and method | Rates displayed before transfer | Yes (depending on delivery option) |

Fees, exchange rates, and delivery times vary based on transfer amount, destination, funding method, and payout option. In 2026, a 1% federal excise tax applies to cash-funded transfers. Bank, debit, and credit card transfers are exempt.

How the new 1% tax on cash remittances affects transfers to Mexico

Starting in 2026, a 1% federal tax applies to certain remittance transfers. The tax applies when you pay with cash, money order, or cashier's check. Transfers funded from a U.S. bank account or with a U.S.-issued debit or credit card are exempt by law.

FAQ

Does Zelle work in Mexico?

No. Zelle does not support international transfers. There is no Mexican bank that offers Zelle for receiving money from the U.S.

What is the best app to send money to Mexico?

It depends on your specific situation. Común offers transfers starting at $2.99 with transparent pricing. Visit comun.app/remittances to learn more.

Remittance service provided by Service UniTeller, Inc. Remittance fees start at $2.99 but may vary. Común Inc. may earn revenue from the conversion of foreign currencies.

Financial Education

Apps like Chime: Best alternatives for 2026

8 min de lectura

Apps like Chime: Best alternatives for 2026

Digital banking apps have changed how many people in the United States manage their money. Instead of visiting physical branches, people can now open accounts, receive direct deposits, send payments, and manage spending directly from their phones.

Among these apps, Chime has become one of the most recognized names in digital banking. However, for many immigrants in the United States, traditional fintech apps may not fully meet everyday financial needs. Some people may need an app that supports ITIN-based onboarding, offers easier ways to send money to Latin America, or provides customer support in both English and Spanish.

What is Chime and why look for alternatives?

Chime is a financial technology company that offers mobile-first banking services through partner banks. Its features include early direct deposit, debit cards, fee-friendly banking options, and automatic savings tools. Some users may look for alternatives because they want: international remittance options, ITIN or passport-based onboarding, bilingual customer support, or cash transfer flexibility.

Comparison of apps like Chime (2026)

| App | Sin comisión mensual | Acepta ITIN/Sin SSN | Soporte en español | Remesas internacionales | Transferencias P2P | Depósito directo anticipado |

|---|---|---|---|---|---|---|

| Chime | Sí | No | No | No | No | Sí* |

| Común | Sí* | Sí | Sí | Sí | Sí | Sí* |

| Current | Sí | No | No | No | Sí | Sí |

| Varo | Sí | Sí (ITIN) | No | No | No | Sí |

*Terms and conditions apply. Verify current requirements with each provider.

Común — The alternative designed for Latino immigrants

Común is a digital financial platform built specifically for the Latino community in the U.S. Unlike Chime and other digital banking apps, Común accepts more than 100 valid Latin American IDs to open an account, offers 24/7 customer support in Spanish, allows sending remittances to Latin America starting at $2.99, and has an app available fully in Spanish. Visit comun.app to learn more.

Varo

Varo accepts ITINs for account opening, making it more accessible for some immigrants. It offers basic banking features without monthly fees. However, it does not offer international remittances or Spanish-language support.

Current

Current offers digital banking with early direct deposit and P2P transfers. However, it does not accept ITINs for account opening and has no Spanish support or international remittances.

Which is the best Chime alternative for immigrants?

It depends on your specific needs. If you need remittances to Latin America, Spanish-language support, and the ability to open an account without an SSN, Común may be the most complete option.

FAQ

Can I open a Chime account without an SSN?

Chime generally requires an SSN to open an account. For immigrants who do not yet have an SSN, there may be better alternatives like Común.

What is the best banking app for Latino immigrants?

Común is designed specifically for Latino immigrants in the U.S. with Spanish support, account opening with Latin American IDs, and international remittances.

Común is a financial technology company and not a bank. Banking services are provided by Community Federal Savings Bank, Member FDIC.

Living in the United States

Websites for finding jobs in the USA: 2026 guide for immigrant workers

8 min de lectura

Websites for finding jobs in the USA (2026 guide for immigrant workers)

An essential guide for finding a job in the USA. The search for a job in a new country can be a challenge, many processes may feel new or unfamiliar. However, in 2026 there are plenty of online resources to help with the process, one of the most commonly used resources is online job platforms. For many Spanish-speaking employment seekers in the USA whether recently arrived or supporting a family, there are employment opportunities available, the key is to know where to find them.

To help with the search, we have created a guide designed as a practical, curated overview of the most relevant websites for finding jobs in the United States. We hope to provide useful context on which platform works best depending on your situation.

The 10 best websites for finding jobs in the USA

1. Indeed

A practical starting point

Among all job platforms in the United States, Indeed continues to be the most widely used, especially for people looking for entry level or widely available opportunities. Its main advantage is volume. It gathers thousands of listings across industries from restaurants, warehouses, cleaning services, retail, to customer service. The platform allows users to apply for many positions directly through the app or website.

However, this same ease of use means competition is high. Users of the platform have reported that, for better chances of success, it is important to apply early and consistently.

Available in Spanish?

Indeed is fully available in Spanish, it is one of the most complete Spanish experiences among all websites for finding jobs in the USA.

2. LinkedIn

For professional and office roles

LinkedIn is more about building a professional presence. Therefore it is very important to have a well structured profile with recommendations and references to all previous experiences to attract potential opportunities.

This platform is commonly used for roles in administration, marketing, finance, and technology. The platform is generally more focused on professional and corporate roles than hourly positions. It is also important to consider that finding a job through it tends to take some time.

Available in Spanish?

LinkedIn is partially available in Spanish. It allows you to change the interface to Spanish, including menus and profile sections. However, most job postings in the USA and recruiter interactions are still primarily in English.

3. Glassdoor

For researching companies

Glassdoor is not just a job board; it is a decision-making tool. While it does include job listings, its real value lies in the information it provides about companies. Users can see salary ranges, employee reviews, and even details about the interview process.

For someone unfamiliar with the U.S. labor market, this can be helpful when evaluating workplace conditions and company culture and help identify companies with better working conditions. Many job seekers use Glassdoor alongside other job search websites in English and Spanish to confirm whether a job is worth pursuing before applying.

Available in Spanish?

Glassdoor is partially available in Spanish. It offers some Spanish interface options and content, but the experience is mixed. The reviews and salary data are often in English, depending on the company. It is still useful, but not fully localized.

4. ZipRecruiter

Faster matching with less effort

ZipRecruiter focuses on simplifying the job search by using technology to match candidates with relevant opportunities. Instead of spending hours browsing, users receive recommendations based on their profile, and in some cases, some employers may contact candidates directly.

This approach is particularly helpful for candidates with some work experience who want to save time and avoid repetitive applications. It reflects how job platforms in the United States are evolving toward more automated and personalized systems.

Available in Spanish?

ZipRecruiter is mostly in English. It is primarily an English-language platform.

5. SimplyHired

Useful for understanding salaries

SimplyHired plays a valuable supporting role. It aggregates listings from multiple sources and provides salary estimates that help job seekers understand what a position typically pays.

For newcomers trying to navigate where to find work in the USA, this information is especially useful. It helps with comparing offers and may help job seekers better understand local ranges.

Available in Spanish?

SimplyHired is partially available in Spanish. It has some Spanish interface support and localized search options. However, like other platforms, many listings remain in English.

6. USAJobs

The official path to government work

USAJobs is the official federal employment portal. It offers access to government positions, which are known for stability, structured hiring processes, and strong benefits.

However, it is important to be realistic about accessibility. Most roles require legal residency or U.S. citizenship, which may limit eligibility for some applicants.

Available in Spanish?

USAJobs offers limited Spanish support. It is mainly in English, as it is the official government portal.

7. FlexJobs

A path to find remote work

As remote work continues to grow, FlexJobs has become one of the most reliable platforms in this space. Unlike larger job boards, it focuses on curated listings, which may help reduce exposure to fraudulent or low-quality listings.

This makes it particularly useful for people looking for flexibility, whether they are freelancers, parents, or simply prefer not to work in a traditional office setting. In the context of websites for finding jobs in the USA, it stands out for prioritizing quality over quantity.

Available in Spanish?

FlexJobs operates almost entirely in English.

8. Upwork

A practical option for remote income

Upwork allows users to work as independent contractors, offering services in areas such as writing, programming, design, and digital marketing. It has become one of the most relevant platforms for remote work, especially as companies increasingly hire global talent.

While it requires time to build a profile and reputation, some users use it to generate freelance or supplemental income and open doors to long-term clients. It is particularly useful for people with digital skills who are looking for flexibility.

Available in Spanish?

Upwork offers a Spanish interface, which makes it more accessible than many remote platforms. However, most clients post jobs in English.

9. Fiverr

For turning skills into income

Fiverr offers a slightly different model from Upwork. Instead of applying to jobs, users create service listings and set their own prices, allowing clients to find them directly.

It is commonly used for creative work and as a source of side income, but it can also grow into a full-time opportunity. Within the broader landscape of job search websites in English and Spanish, Fiverr stands out for its flexibility and accessibility.

Available in Spanish?

Fiverr also supports Spanish in its interface. Since you create your own service listings, you can write them in Spanish, English, or both, which gives you flexibility depending on your target clients.

10. The Muse

A more curated, culture-focused option

The Muse is smaller than other platforms but offers a more curated experience. It focuses on companies that prioritize workplace culture and transparency, giving candidates a clearer idea of what to expect.

This makes it particularly appealing for younger professionals or those looking for a better long-term fit rather than just immediate employment. While it may not be the first stop for most job seekers, it can be a valuable complement to larger platforms.

Available in Spanish?

The Muse is primarily an English-language platform with no full Spanish interface.

Choosing the right platform for your situation

These platforms are useful within their unique context, the key to making the most out of them is understanding what they offer and how they fit in your situation. Someone looking for quick, entry-level work will likely benefit most from Indeed, while a candidate pursuing a long-term professional career should prioritize LinkedIn. Those interested in flexibility or remote income may find better results through FlexJobs, Upwork, or Fiverr, while individuals seeking long-term stability may consider USAJobs if they meet the requirements.

In practice, the most effective strategy is not to rely on a single platform. Combining two or three of these tools creates a more balanced approach and may improve job search efficiency.

How to apply without an SSN or with an ITIN

When exploring websites for finding jobs in the USA, one practical question often comes up early in the process: what happens if you don't yet have a Social Security Number (SSN)? In most formal employment situations, an SSN is required because employers use it for payroll and tax reporting. However, during the application stage, many platforms still allow you to apply without entering one.

If you already have legal work authorization but are waiting for your SSN, you can:

- Typically move forward in the hiring process, if the employer allows, and provide the number later

- In some cases, employers may accept an Individual Taxpayer Identification Number (ITIN) for tax purposes (although it does not replace work authorization)

The key distinction is that an ITIN allows you to comply with tax obligations, but it does not grant permission to work.

Requirements can vary depending on the employer and the type of role, therefore it is important to confirm what documentation will be needed once you move forward in the hiring process.

Tips for preparing your application

Using the right job platforms in the United States is the first part of the process. How you present yourself still plays a major role in whether you get a response.

- A strong resume should be clear, concise, and tailored to the type of job you are applying for

- In the U.S., resumes are typically one page and focus on skills and results rather than long descriptions

- Adjusting your resume to include keywords from the job description may help resumes align with automated application systems used by some employers

When it comes to interviews, preparation is just as important:

- Employers often expect candidates to explain their experience clearly and give examples of past work

- If you are not fluent in English, practicing common questions in advance can help you feel more confident

Applying regularly, following up when appropriate, and staying organized throughout the process may help improve consistency throughout the job search.

After you get the job: getting paid

Once you are successful and you find work in the United States, it is important to know how and where you are getting paid. Most employers rely on direct deposits, which requires access to a U.S. bank account. For many immigrants, this can be a challenge. Some financial institutions and fintech platforms offer products designed for individuals who may have limited access to traditional banking services. From traditional banks to digital platforms it's important to learn about their requirements and their offers. For example, with Común you can open a debit account using a passport or more than 100 valid Latin American IDs and Común's app is available in Spanish.

Frequently Asked Questions

Do I need a work permit to work in the United States?

Yes. To work legally in the U.S., you must have valid work authorization. This typically comes in the form of a work permit (Employment Authorization Document, or EAD) or a visa that allows employment.

What types of work permits are available for immigrants?

There are several common pathways depending on your situation. Temporary work visas like the H-2A (agricultural work) and H-2B (seasonal non-agricultural work) are frequently used. Professional visas such as the H-1B apply to specialized roles, while other options like TPS (Temporary Protected Status) or asylum-based work permits may apply depending on your country of origin and circumstances.

Each option has specific requirements, so it is important to verify eligibility with the official authorities.

Can I work in the United States if I don't speak English?

Yes, it is possible. Many jobs, especially in construction, cleaning, manufacturing, agriculture, and restaurants do not require advanced English. In cities with large Latino populations, it is common to find Spanish-speaking work environments.

However, improving your English can significantly expand your opportunities and increase your earning potential over time.

What are employment agencies?

Employment agencies, also known as staffing agencies, act as intermediaries between companies and job seekers. They help match candidates with available positions, often for temporary, seasonal, or entry-level roles.

For many newly arrived immigrants, these agencies may help some job seekers connect with available opportunities, especially if someone does not yet have a strong professional network in the United States.

Final thoughts

The key to navigating the U.S. job market in 2026 is not just knowing the websites for finding jobs in the USA, but understanding how to use them strategically. Each platform serves a different purpose, and choosing the right one may help better organize search and identify opportunities aligned with goals and experience. We wish you the best of luck in your job seeking process!

Financial Education

How to Emigrate to the United States: Practical Guide and Helpful Tips

8 min de lectura

Complete Guide to Emigrating to the United States

Have you thought about alternatives to build a better future? You probably share the dream of thousands who long to emigrate to the U.S. in search of job and financial stability. Although the idea is tempting, it’s important to do it in an orderly and legal way to avoid issues with the U.S. government.

Beyond better job opportunities, people emigrate seeking education, family reunification, and safety.

The process to live legally in the U.S. can be overwhelming and confusing. This guide explains, step by step, how to emigrate to the United States to work, study, and reside.

Main Options to Emigrate to the United States

First, understand the different visa categories you can apply for to legally enter the U.S.—whether for work, family ties, or other categories.

These are the visa categories:

Employment

If your goal is to find job opportunities in the United States, you need to understand the work visa options.

- H-1B visa: for specialized professionals with a university degree or equivalent experience.

- H-2B visa: temporary non-agricultural workers.

- H-2A visa: temporary agricultural workers.

- TN visa: (NAFTA/USMCA) for Mexican and Canadian citizens in specific professions.

- EB-5 visa: for investors able to create at least 10 U.S. jobs. Also a pathway to permanent residence.

Family

Another path is the family-sponsored Green Card, which lets U.S. citizens and permanent residents help certain relatives obtain legal status.

U.S. citizens may petition for a spouse, unmarried or married children, parents, and siblings; permanent residents may petition for a spouse and unmarried children under 21.

Processing times vary but can be around 18 months. In general, the card is issued with a 10-year validity.

Visa Lottery

If you don’t fit employment or family categories, you can consider the Diversity Visa (DV Lottery), which grants 55,000 lawful permanent resident visas to nationals from countries with low U.S. immigration rates.

These are the requirements to apply:

- Be from an eligible country.

- Have a high school education and at least two years of experience in an occupation.

- Complete the online form during October–November.

Other options

Lastly, there are other alternatives for foreign nationals who don’t fit the categories above.

- Student visa (F-1 or M-1).

- Exchange visitor visa.

- Asylum or refugee status.

- Humanitarian parole or special programs.

Step-by-Step to Start Your Immigration Process

Below is the visa application process step by step.

Step 1. Research the most viable path for your profile.

First, analyze your goals in the U.S. and which visa category best fits your profile.

Step 2. Estimate process costs and initial cost of living in the U.S.

Immigrant visa costs vary by category. For example, in family sponsorship, Form I-130 or I-140 ranges from $535 to $700.

Check exact fees on the official U.S. Citizenship and Immigration Services website.

Step 3. Gather required documents (certificates, passports, diplomas, records, proof of income, etc.).

Each visa type requires specific documents; below is a general list of the most important items.

Valid passport.

- DS-160 (temporary visas) or DS-260 (immigrant visas).

- Proof of consular fee payment.

- Recent visa-style photo (2x2 inches).

- Job offer letter.

- USCIS employment authorization document.

- Academic certificates, diplomas, professional degrees.

- Proof of work experience.

- Proof of financial solvency or bank statements.

Step 4. If needed, improve your English before emigrating.

While the immigrant community is large, you’ll still need at least basic English to communicate.

Step 5. Check USCIS official sources to confirm current forms and fees.

Forms and fees vary by visa type. Always consult USCIS official information.

Also keep these practical tips in mind to avoid common mistakes.

- Avoid unlicensed consultants.

- Don’t make payments on unofficial sites. Make sure URLs end in .gov.

- Keep digital copies of all official documents for easy backup.

State Options for Emigrating to the U.S. and Costs to Consider

The next key step is choosing the state where you’ll arrive once you get your visa. This choice can directly impact your success due to the cost of living, job opportunities, and minimum wage.

Several states are attractive due to job variety, access to services, and support networks.

Here is a comparative table of some of the U.S. states for immigrants.

State

Average cost to rent a room

Average cost to rent a family home

State or federal minimum wage

Texas

$1,130

$1,400

Federal minimum wage $7.25 per hour

California

$2,600

$3,500

$14.00 per hour

Florida

$1,290

$2,000

$11.00 per hour

New York

$2,125

$2,300

$15.50 per hour

Illinois

$1,140

$1,300

$15.00 per hour

Arizona

$1,171

$1,400

Federal minimum wage $7.25 per hour

Helpful Tips for a Successful Transition

Emigrating requires financial, legal, and emotional preparation. These tips help you transition more smoothly.

- Once in the U.S., open a checking account to facilitate payments and salary deposits.

- Create an initial budget for the first 3–6 months.

- Line up temporary housing before traveling—family or friends if possible.

- Learn how the healthcare system and insurance work.

- Learn how credit history works and how to start building it.

Build Your New Financial Life in the U.S. with Común

You’re one step closer to starting a new life in the U.S. Once there, you’ll need a reliable service to manage your money.

Meet Común, the financial platform in the U.S.!

Open a checking account with qualifying ID from your home country and send money to Latin America with clear, competitive fees.

Open your Común checking account and take the first step toward financial stability in the U.S.

Frequently Asked Questions (FAQ)